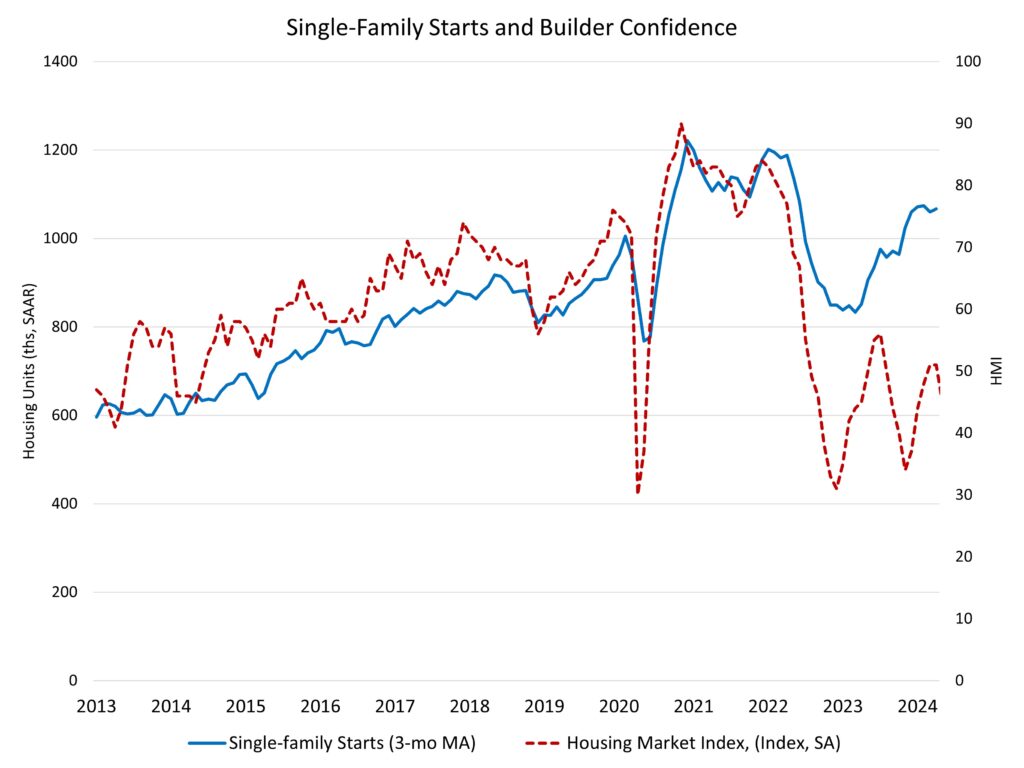

Single-family starts remained flat in April as mortgage interest rates moved above 7% last month and builders continued to face tight lending conditions.

Overall housing starts increased 5.7% in April to a seasonally adjusted annual rate of 1.36 million units, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau.

The April reading of 1.36 million starts is the number of housing units builders would begin if development kept this pace for the next 12 months. Within this overall number, single-family starts decreased 0.4% to a 1.03 million seasonally adjusted annual rate. However, this pace is 17.7% higher than a year ago. On a year-to-date basis, single-family starts are up 25.7%, totaling 335,600. Despite higher interest rates, demand for new single-family housing continues to be supported by low levels of resale inventory. Lower interest rates will provide additional support for single-family home building by reducing rates on construction and development loans, when the Fed begins its eventual easing cycle.

The multifamily sector, which includes apartment buildings and condos, increased on a monthly basis 30.6% to an annualized 329,000 pace. However, this is 32% lower than a year ago. Moving forward, the multifamily market will see additional declines for construction volume, while the pace of completions remains elevated. This additional rental supply will help lower shelter inflation, which is the last leg of the inflation policy challenge.

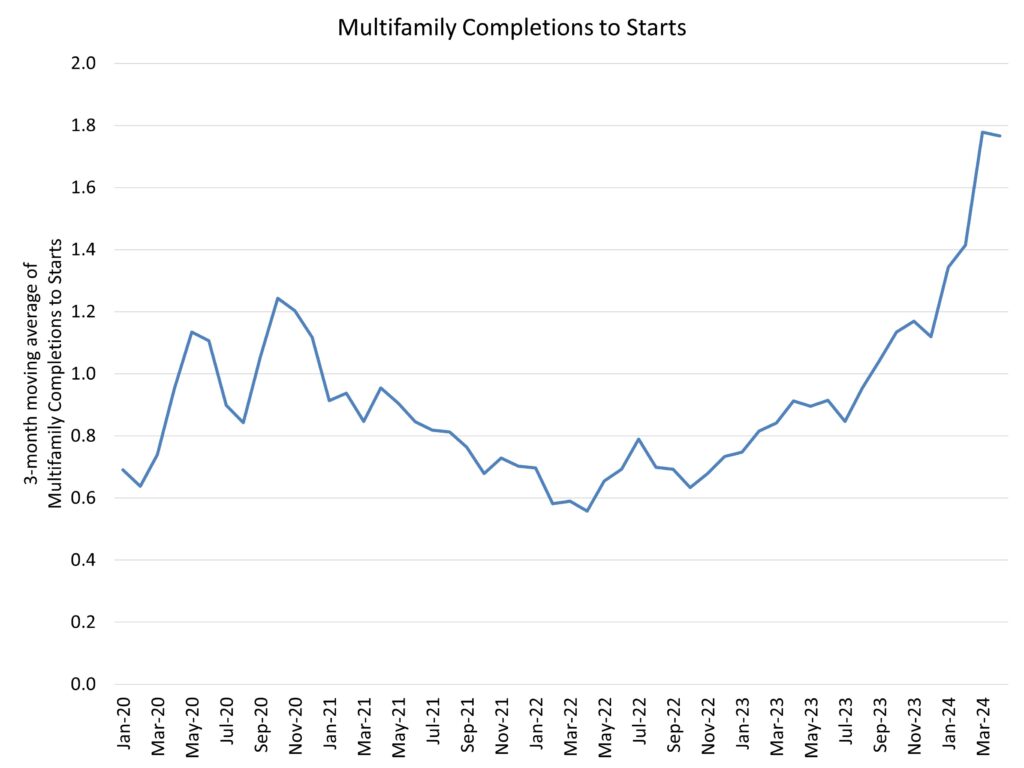

April marked the fifth consecutive month for which the seasonally adjusted rate of multifamily completions was above 500,000. The ongoing reversal within multifamily construction – from an accelerated pace of starts to an accelerated pace of completions – can be seen on the chart below. At the end of 2020, the rate of multifamily construction starts was roughly equal to the rate of completions. For all quarters after this period until the third quarter of 2023, apartment construction starts exceeded the rate of completions. With the third quarter of 2023, this reversed and since September 2023, there have been more multifamily completions than starts, thus reducing the total number of multifamily units under construction. For April 2024, the ratio of multifamily completions to starts was 1.8 on a three-month moving average.

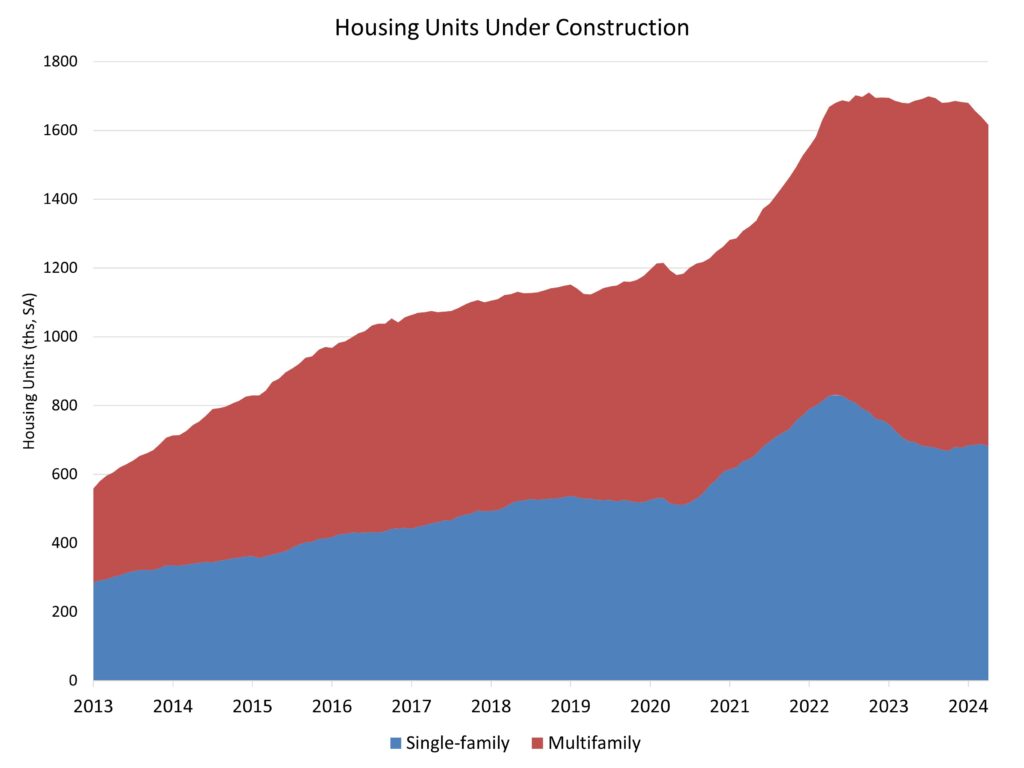

After peaking in July 2023 at 1.02 million apartments under construction, active multifamily units under construction declined to 934,000 in April. This is 4.2% lower than a year ago. In April, there were 674,000 single-family homes under construction, the highest count since November 2023 and down just 2.1% year-over-year.

On a regional and year-to-date basis, combined single-family and multifamily starts are 24.5% lower in the Northeast, 11.0% higher in the Midwest, 1.8% higher in the South and 8.4% higher in the West.

Overall permits decreased 3.0% to a 1.44 million unit annualized rate in April. Single-family permits decreased 0.8% to a 976,000 unit rate; this is the lowest pace since August 2023. Multifamily permits decreased 7.4% to an annualized 464,000 pace.

Looking at regional data on a year-to-date basis, permits are 9.3% higher in the Northeast, 8.5% higher in the Midwest, 2.8% higher in the South and 0.2% higher in the West.

An important technical note: Census and HUD provided revisions for the construction data this month, some ranging back to 2017.

Notice of Revision: With this release, unadjusted estimates of housing units authorized by building permits for January 2022 through December 2023 have been revised. Also, seasonally adjusted estimates of housing units authorized by building permits have been revised back to January 2017, and seasonally adjusted estimates of housing units authorized but not started, started, under construction, and completed have been revised back to January 2019. All revised estimates are available on our website.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.