As examined in a previous post, homeownership plays an integral role in a household’s accumulation of wealth. This article further discusses the role of homeownership and examines the difference between homeowner and renter household balance sheets across assets, debt, and net worth.

Households who own a primary residence (homeowners) build primary residence equity, while renters have zero residence equity. In the third quarter of 2023, CoreLogic’s homeowner report analysis detailed that U.S. homeowners with mortgages have seen their equity increase by a total of $1.1 trillion, a gain of 6.8% from the same period in 2022. In addition to primary residence equity, households who own a primary residence almost always own other assets as well.

In contrast, households who do not own a primary residence (renters) neither accumulate wealth from home price appreciation, nor do they benefit from primary residence equity gains by paying down a home mortgage. Moreover, renters typically own a much smaller amount of other assets in aggregate than homeowners.

Both home equity and non-residence equity account for the wealth gap between homeowners and renters. It is useful to keep in mind that almost all households will spend time as a renter and time as an owner. Prior NAHB analysis1 indicates about 9 out of 10 households will be homeowners during some period of their lifetime. As such, while homeownership is key pathway for wealth accumulation, the rental market plays a role in this process as well, as most households will rent before they own a home.

ASSETS:

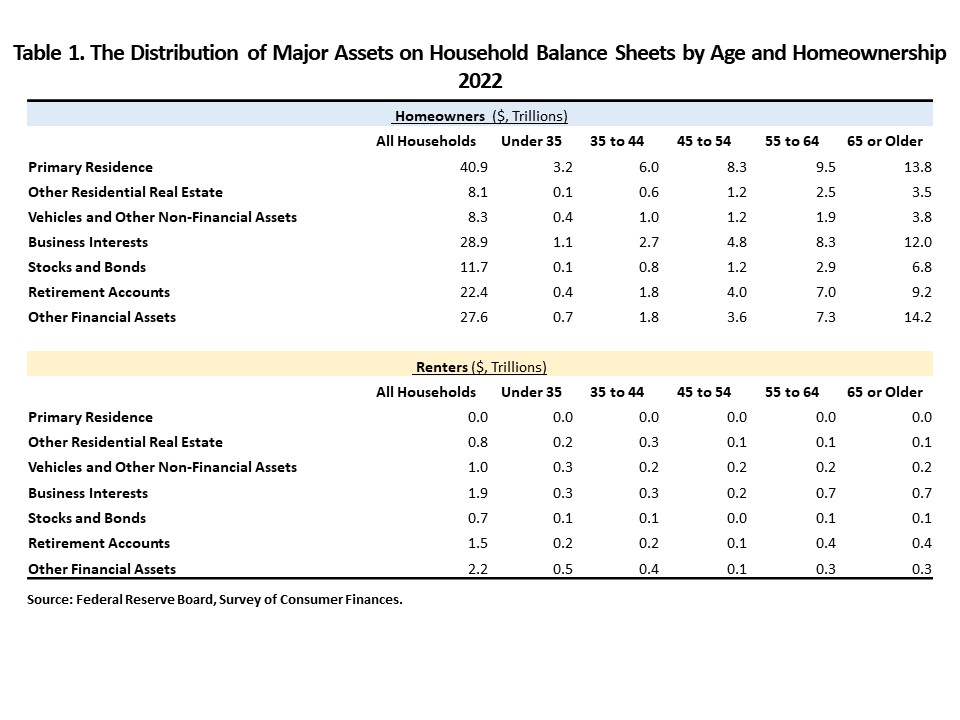

In 2022, while almost every family owned some assets, homeowners own the vast majority of assets in aggregate. An analysis of the Survey of Consumer Finances (SCF) suggests that the households who owned a primary residence own most other assets in sum, such as other residential real estate2, vehicles, other non-financial assets3, business interests, stocks and bonds, retirement accounts, and other financial assets4. This is shown in Table 1 below.

In contrast, renters who do not own a primary residence do not own as many other assets as homeowners. For example, in aggregate, homeowners owned 16 times more stocks and bonds than renters, 15 times more business interests and retirement accounts than renters.

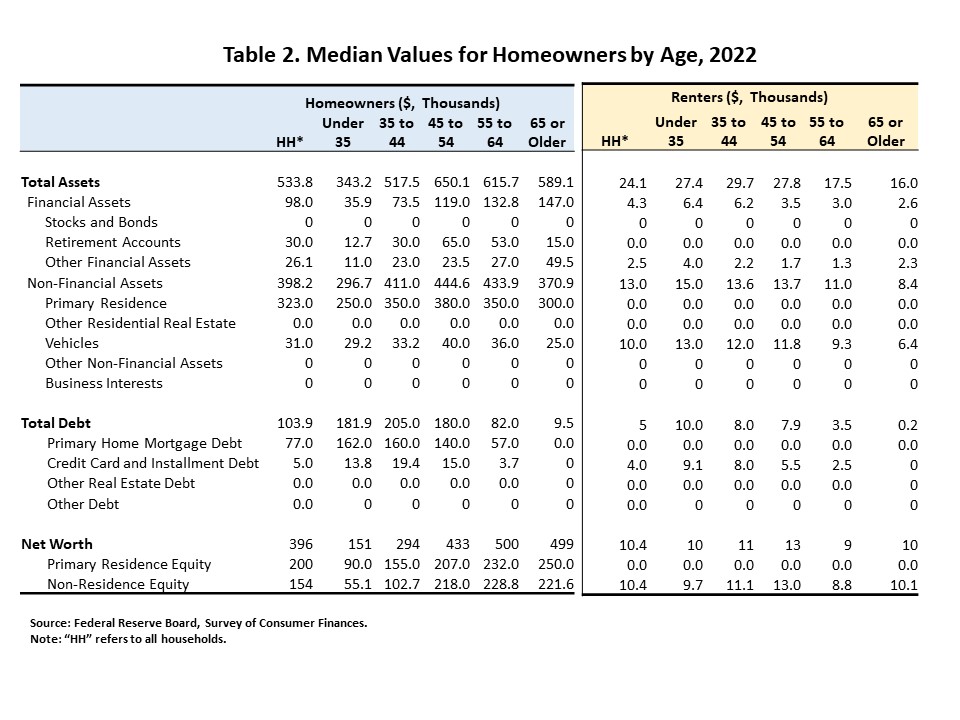

Table 2 presents median values of assets, debt, and net worth for all these homeowners and renters by age categories in 2022. Homeownership and housing wealth are strongly associated with age. The median value of the primary residence rose for homeowners aged between 35 and 44, reached the peak for homeowners aged 45 and 54, before declining for those aged 55 and above. Meanwhile, the median value of homeowners’ other financial assets continued to rise across these age categories. The median value of retirement accounts increased to $65,000 for homeowners aged between 45 and 54 and decreased as age increased.

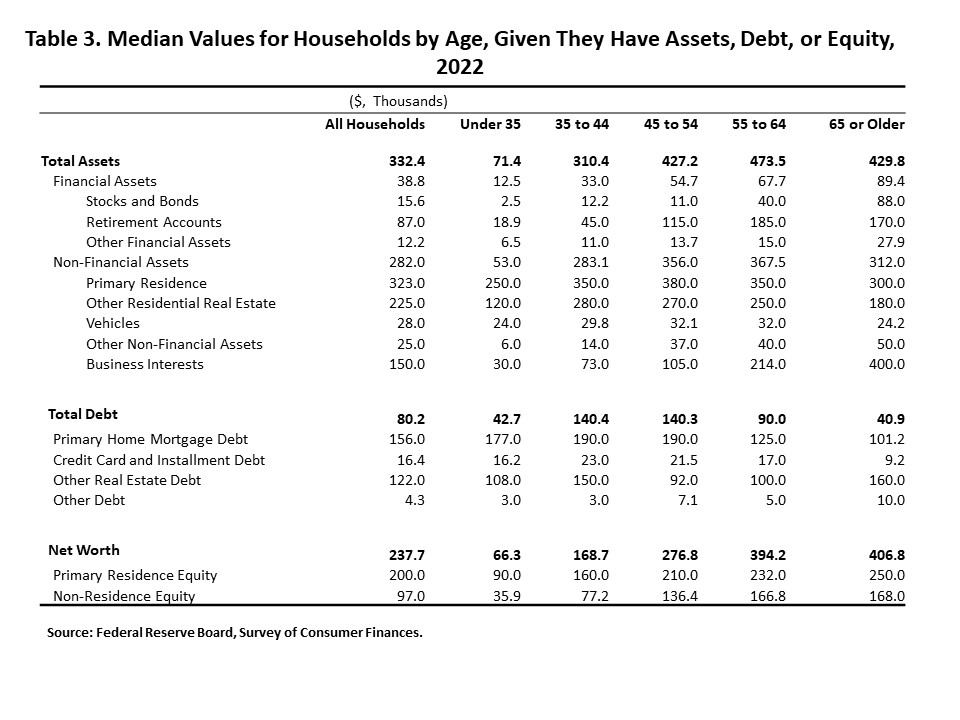

At the same time, the median value of business interests, other non-financial assets, and stocks and bonds among homeowners remained zero, indicating that fewer than half of homeowners own these assets at any age cohort. While Table 1 suggests that the owners of these assets are more likely to be homeowners, Table 2 indicates that a minority of homeowners own such assets. However, among households that owned these assets, the median value of business interests, other non-financial assets, and stocks and bonds grew over the entire age categories, as illustrated by Table 3 below.

For renters, more than half of renters owned other financial assets, but they did not accumulate as they aged. Noticeably, fewer than half of renters owned retirement accounts, other residential real estate, other non-financial assets, and business interests at any age cohort. When renters were 65 or older, the median value of their financial assets and non-financial assets dropped by almost half from the median value when they were under 35.

DEBT:

On the debt side of homeowners’ balance sheets, the value of the primary home mortgage debt was the largest liability faced by homeowners. However, the median value of mortgage debt declined between the 35 to 64 age categories. More than half of homeowners above the age of 65 did not have mortgage debt (nor a balance on any of the other major debt categories).

For renters, the value of credit card and installment debt was the largest liability in their debt category. The median value of credit card and installment debt declined between the 35 to 64 age categories and was zero for renters aged 65 or older.

NET WORTH:

Net worth, the measure of households’ wealth, is the difference between families’ assets and liabilities. An analysis of the 2022 SCF found that homeowners had a median net worth of $396,000, while renters had the median net worth of just $10,400. Thus, homeowners are wealthier than renters.

Among homeowners, the primary residence equity was the largest category of their net worth. However, for renters, the non-primary residence equity was the larger portion of their net worth, reflecting the accumulation of other assets by renters in their life stages, as illustrated in Table 2.

Across homeowners, the median amount of primary residence equity rose successively with age, largely reflecting a lower amount of mortgage debt as opposed to a higher home value.

In 2022, the median net worth for homeowners was about 38 times the median net worth for renters. Excluding the primary residence equity from net worth, the median non-residence equity of homeowners was 15 times that of renters.

Note:

1 Ford, C. (2019). “Lifetime Homeownership and Homeownership Survival Rates Using the National Longitudinal Survey of Youth,” NAHB Special Studies, November 1, 2019.

https://www.nahb.org/-/media/1057BA30B7A94167A26D3AC1F7A6B498.ashx

2 Other residential real estate includes land contracts/notes household has made, properties other than the principal residence that are coded as 1-4 family residences, time shares, and vacation homes.

3 Other non-financial assets defined as total value of miscellaneous assets minus other financial assets.

4 Other financial assets include loans from the household to someone else, future proceeds, royalties, futures, non-public stock, deferred compensation, oil/gas/mineral investments, and cash, not elsewhere classified.

5 According to the SCF, the term “families”, used in the SCF, is more comparable with the U.S. Census Bureau definition of “households” than with its use of “families”. More information can be found here: https://www.federalreserve.gov/publications/files/scf17.pdf.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

Construction loans play a crucial role in facilitating homeownership by providing funding for building or renovating homes, thereby contributing to the accumulation of wealth through property ownership. Understanding these disparities underscores the importance of accessible financing options, like construction loans, in promoting broader access to homeownership and wealth accumulation.