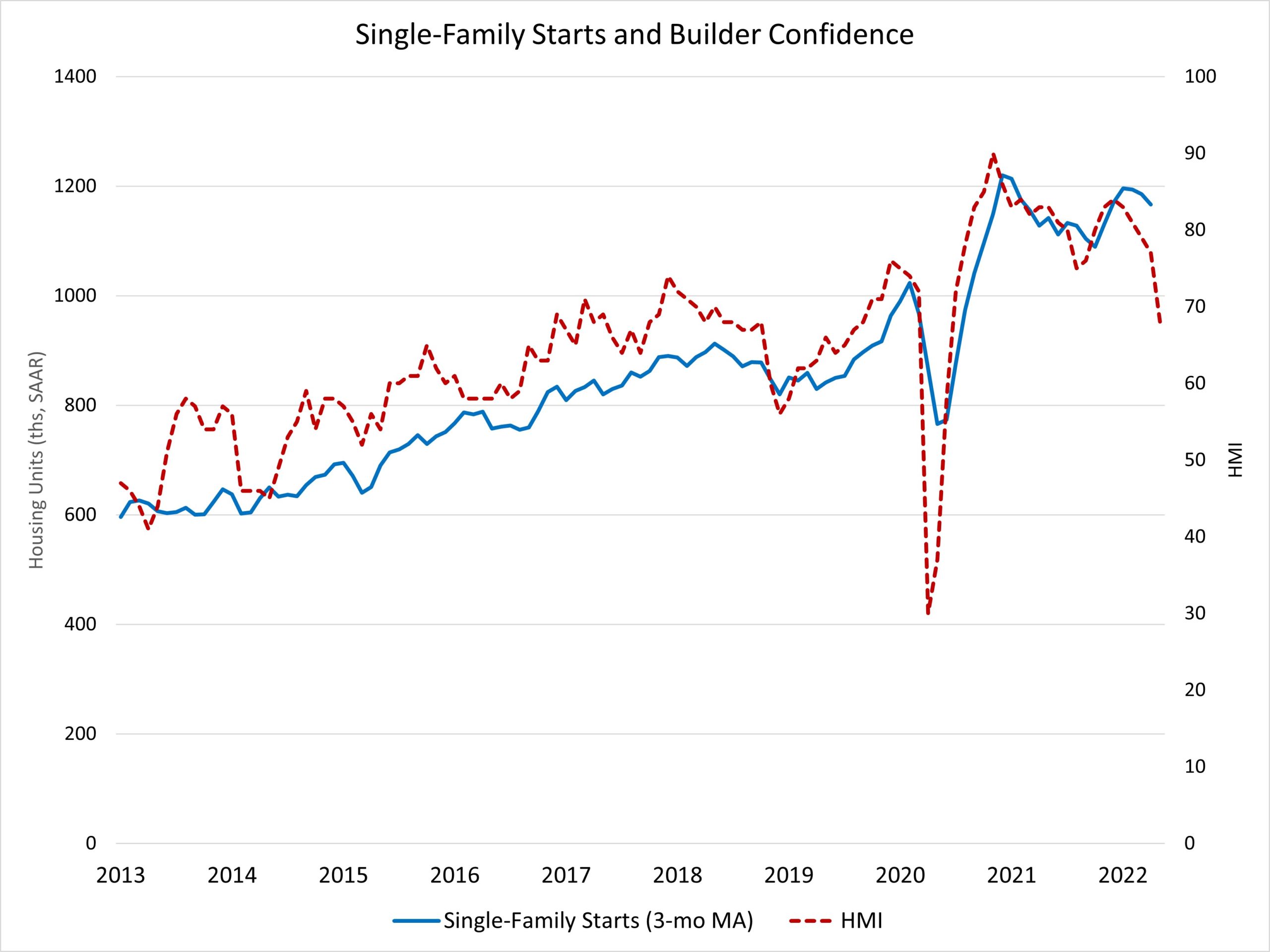

Single-family starts declined in April, as higher interest rates weighed on housing affordability, producing a fifth straight decline for the NAHB/Wells Fargo HMI. Additionally, the cost and availability of materials, lumber, labor and lots remain key supply-side headwinds. Single-family permits decreased 4.6% to a 1.11 million unit rate in April. Nonetheless, the resale market lacks inventory, which is supporting demand for new construction.

Overall housing starts were effectively flat at 1.72 million units, according to a report from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau. The April reading of 1.72 million starts is the number of housing units builders would begin if development kept this pace for the next 12 months.

Within this overall number, single-family starts decreased 7.3% to a 1.1 million seasonally adjusted annual rate. The multifamily sector, which includes apartment buildings and condos, continued to gain ground, rising 15.3% to a strong 624,000 annual rate.

Due to supply-chain effects, there are 153,000 single-family units authorized but not started construction—up 8.5% from a year ago.

In May single-family builder confidence decreased 8 points to a level of 69, according to the NAHB/Wells Fargo Housing Market Index (HMI). After peaking at a level of 90 in November 2020, builders have reported ongoing concerns over elevated lumber, OSB and other construction costs, as well as delays in obtaining building materials. The sharp rise in mortgage interest rates at the start of 2022 has also had an impact on sales expectations. Consequently, the market has likely reached an inflection point whereby a new volume trend based on current affordability conditions must be found. This will mean a shift lower for single-family demand and a step up in demand for apartment construction. The April data is consistent with this impact.

On a regional and year-to-date basis, combined single-family and multifamily starts are 6.3% higher in the Northeast, 5.2% higher in the Midwest, 13.3% higher in the South and 8.3% higher in the West.

Overall permits decreased 3.2% to a 1.82 million unit annualized rate in April. Single-family permits decreased 4.6% to a 1.11 million unit rate. Multifamily permits decreased 1.0% to an annualized 709,000 pace.

Looking at regional permit data on a year-to-date basis, permits are 4.9% lower in the Northeast, 4.0% higher in the Midwest, 3.5% higher in the South and 1.3% higher in the West.

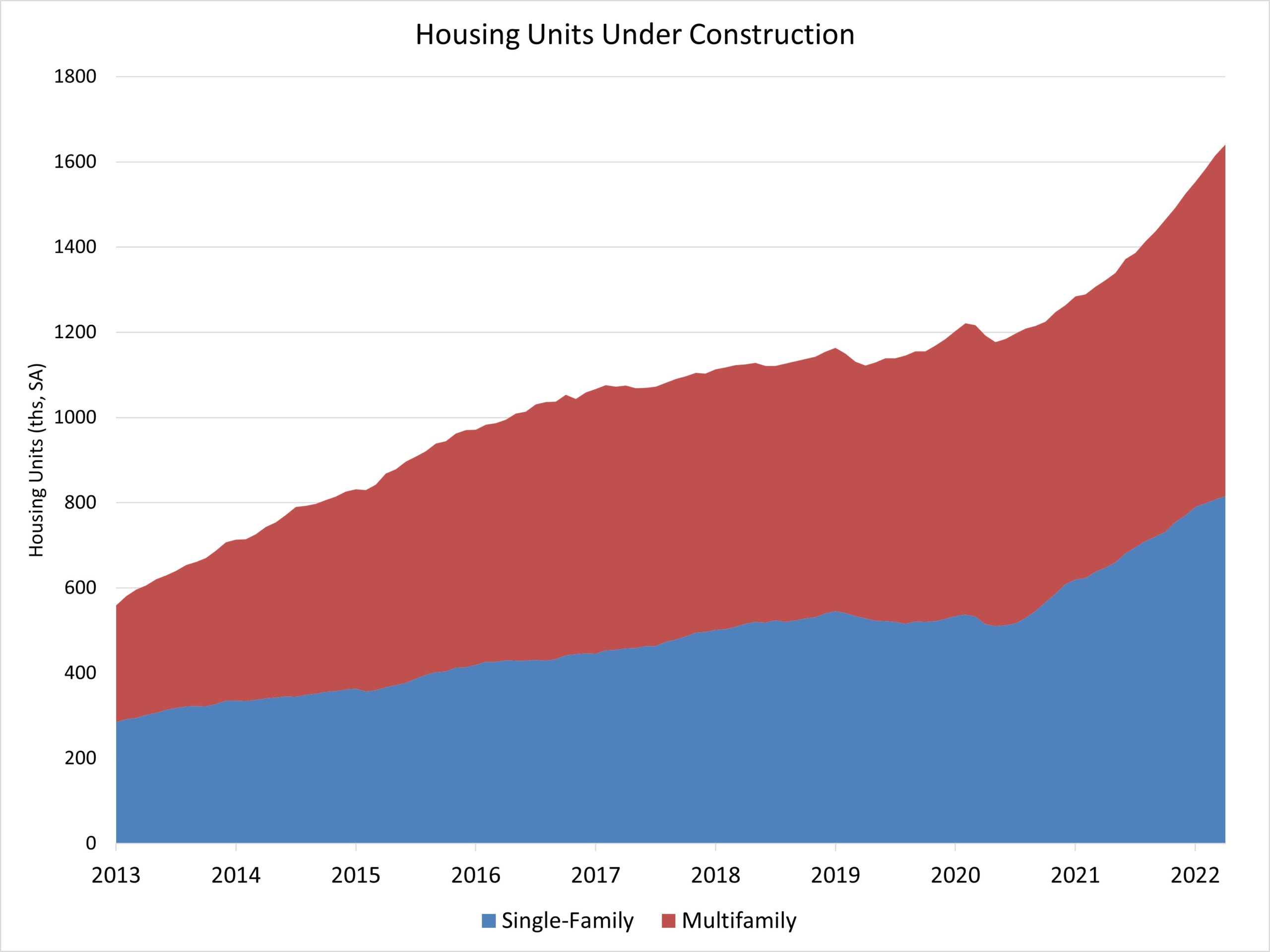

As an indicator of the economic impact of housing and as a result of accelerating permits and starts in recent quarters, there are now 815,000 single-family homes under construction. This is 26% higher than a year ago. There are currently 826,000 apartments under construction, up 22% from a year ago. Total housing units now under construction (single-family and multifamily combined) is 24% higher than a year ago. The number of units under construction is rising on both the total volume of construction, as well as longer construction times. However, this growing inventory base does imply an end to the post-covid growth rates for residential construction.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.