An earlier post revealed that 67% of buyers who were actively engaged in the process of finding a home in the final quarter of 2021 have spent 3+ months searching for a home without success. The inability to find a home they could afford once again became the most common reason (41%) these long-time searchers could not buy a home. The inability to find a home with desirable features (39%) was second. In third place, 35% attributed their lack of success to getting outbid by other buyers’ offers. The latter share is down from 45% a quarter earlier, probably due in part to less competition from buyers discouraged by dwindling affordability.

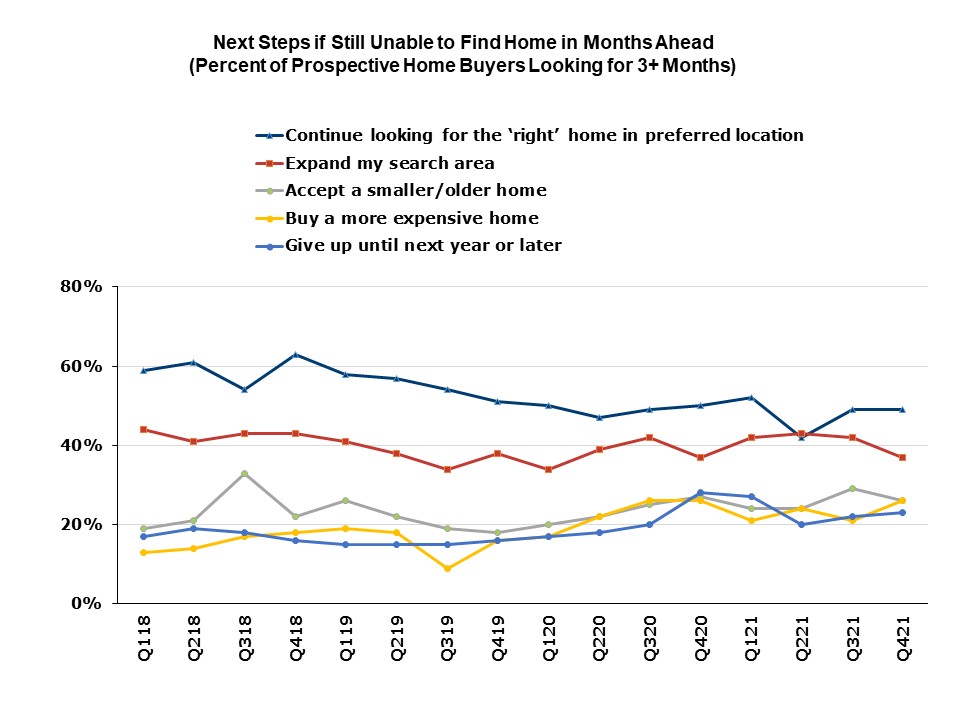

When asked what they are most likely to do next if still unable to find a home in the next few months, 49% of active buyers searching for 3+ months said they will continue looking for the ‘right’ home in the same location, unchanged from the third quarter. The share that will buy a more expensive home rose during this period, from 21% to 26%.

Meanwhile, the share who plan to give up their home search until next year or later has begun to rise again, from 20% in the second quarter of 2021 to 23% in the final quarter of the year.

The Housing Trends Report is a research product created by the NAHB Economics team with the goal of measuring prospective home buyers’ perceptions about the availability and affordability of homes for-sale in their markets. The HTR is produced quarterly to track changes in buyers’ perceptions over time. All data are derived from national polls of representative samples of American adults conducted for NAHB by Morning Consult. Results are seasonally adjusted. A description of the poll’s methodology and sample characteristics can be found here. This is the final post in a series of six highlighting results for the fourth quarter of 2021. See previous posts on plans to buy, new vs. existing preference, housing availability, housing affordability, and active buyers.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

In my opinion, higher interest rates and the threat of significantly higher rates is playing a major role in shrinking the market.

To most buyers the sales price serves little more than

guide to determine what they will look at. This is because of the multiple variable that determine monthly housing expense, such as mortgage interest rates, taxes

and insurance costs, all generally unknown when shopping.

The purchase decision is nearly always made based on the amount of the initial cash investment and total monthly housing expense. Mortgage interest rates have, by far, the greatest affect on those monthly costs and to a kisser degree, the cash investment required.

Most of those financially astute enough to have gathered the cash to invest in a new home understand that rates are rising and that the FED’S efforts to control runaway inflation will expose most buyers of new homes to the risk of significantly higher rates over the typical 6 to12 months their new home is under construction. If you research what mortgage rates were the last time the inflation rate was over 7% the results will scare you.

The industry has had an excellent year and the backlog of sales is enormous because of sales volume and supply related construction delays. My opinion is that builders should be working on plans to identify potential mortgage problems within their backlog and to deal with them to avoid loosing a significant number of sales from the backlog.