Due to tightened monetary policy, the count of total job openings for the entire economy has trended lower in recent months. This is consistent with a cooling economy that is a positive sign for future inflation readings. However, the December data showed an uptick due to stronger than expected GDP growth for the fourth quarter of 2023.

In December, the number of open jobs for the economy increased to 9.0 million. This is notably lower than the 11.2 million reported a year ago. NAHB estimates indicate that this number must fall back below 8 million for the Federal Reserve to feel more comfortable about labor market conditions and their potential impacts on inflation.

While the Fed intends for higher interest rates to have an impact on the demand-side of the economy, the ultimate solution for the labor shortage will not be found by slowing worker demand, but by recruiting, training and retaining skilled workers. This is where the risk of a monetary policy mistake had some risk of arising. Good news for the labor market does not automatically imply bad news for inflation.

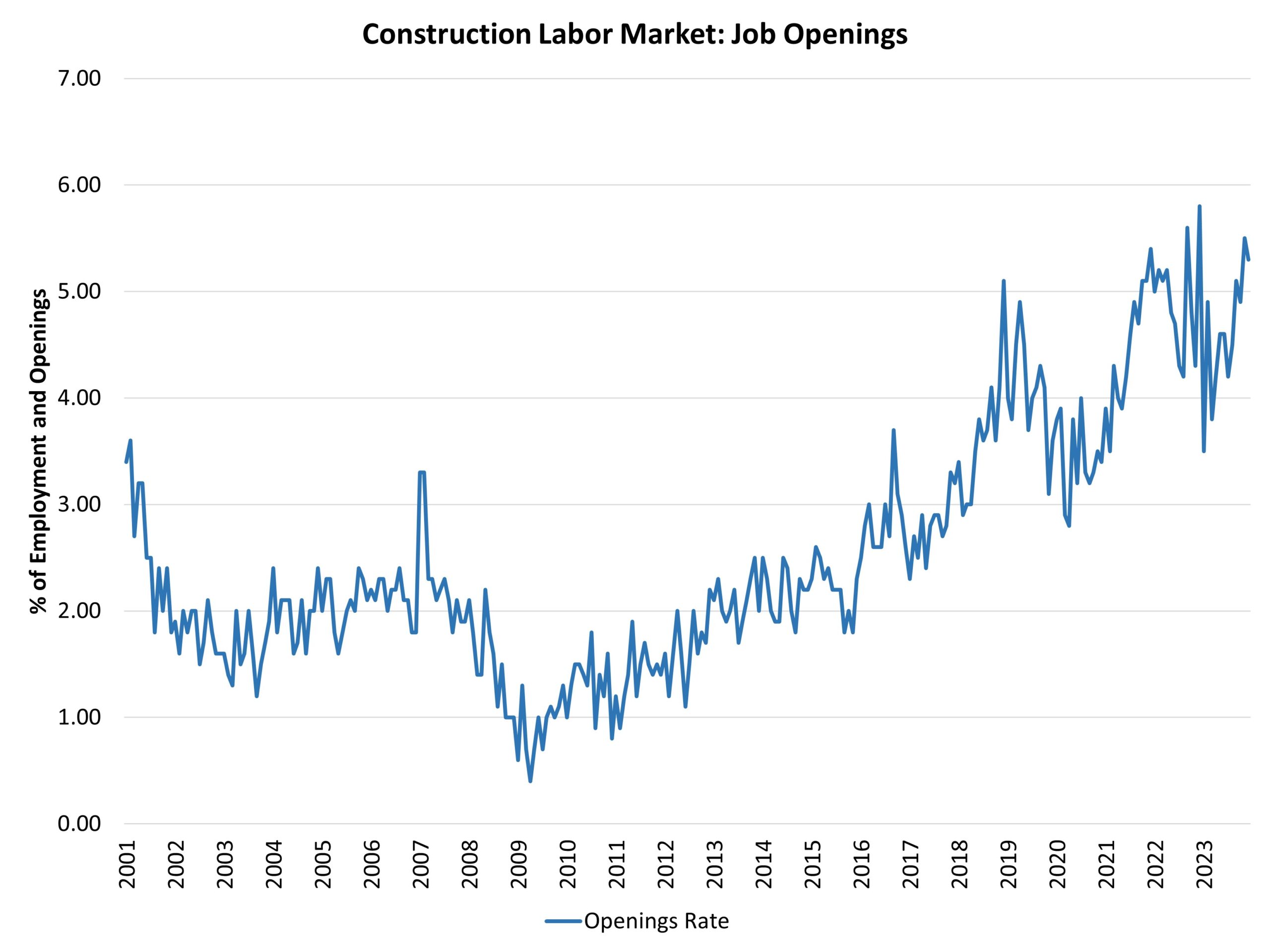

The number of open construction sector jobs was relatively unchanged in the most recent data, declining from 470,000 in November to 449,000 in December. The count was 488,000 a year ago, during an outlier month of strong data. The construction job openings rate decreased slightly to 5.3% in December. The recent, increasing trend indicates an ongoing skilled labor shortage for the construction sector.

The housing market remains underbuilt and requires additional labor, lots, and lumber and building materials to add inventory. Hiring in the construction sector increased to a 4.6% rate in December after 4.5% in November. The post-virus peak rate of hiring occurred in May 2020 (10.4%) as a post-covid rebound took hold in home building and remodeling.

Construction sector layoffs were steady at a 2.1% rate in December after 2.1% in November. In April 2020, the layoff rate was 10.8%. Since that time, the sector layoff rate has been below 3%, with the exception of February 2021 due to weather effects and March 2023 due to some market churn.

Looking forward, attracting skilled labor will remain a key objective for construction firms in the coming years. While a slowing housing market will take some pressure off tight labor markets, the long-term labor challenge will persist beyond the ongoing macro slowdown.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.