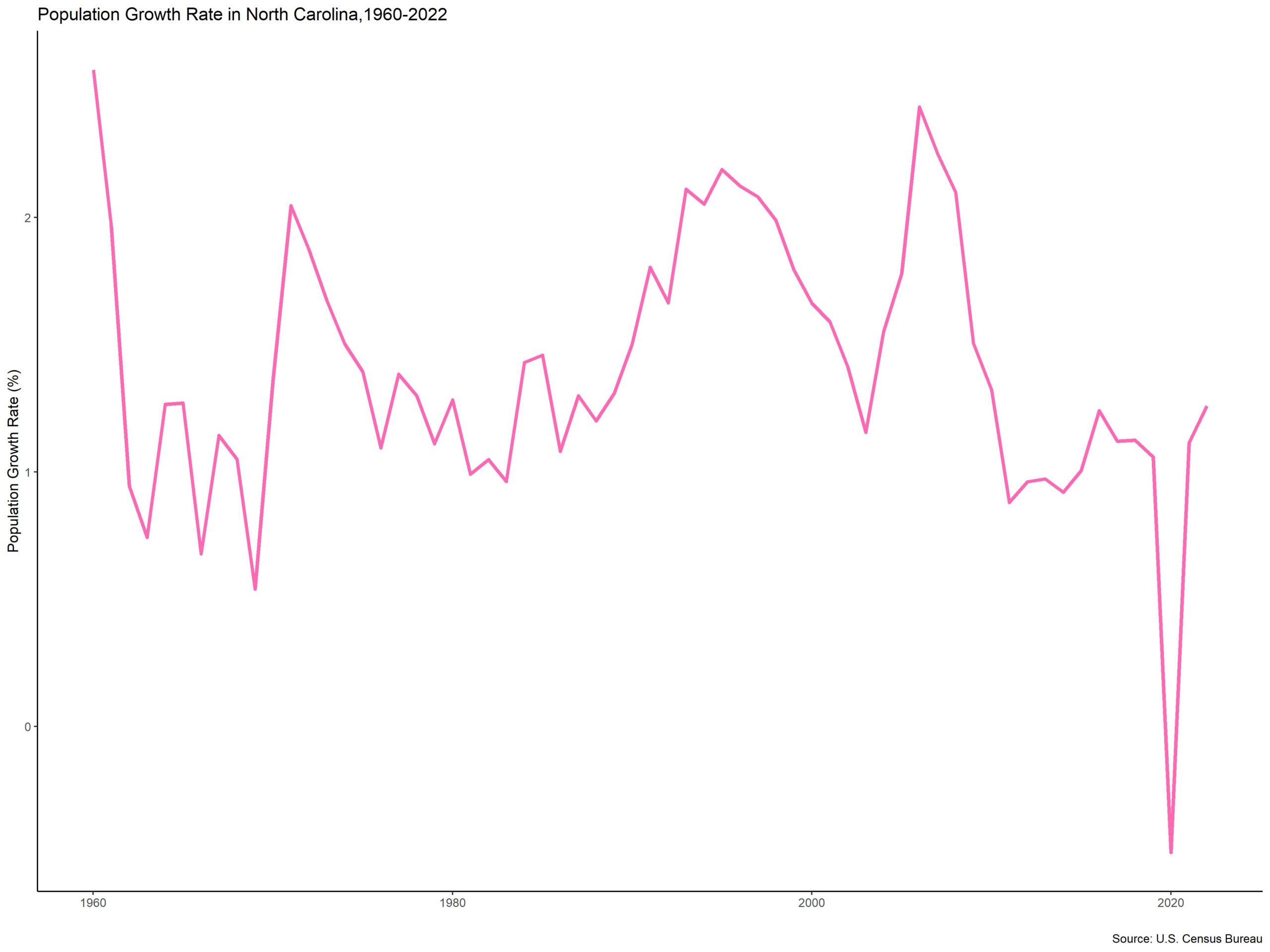

The population of North Carolina rebounded strongly from a brief period of negative growth the state experienced in 2020 due to the COVID-19 pandemic.

North Carolina’s population grew at a rate of 1.3% between 2021 and 2022, the ninth fastest of any state. By count, North Carolinas population increased by 133,088, the 3rd largest nominal increase in the U.S. North Carolina was one of four states to have a nominal population increase above 100,000 between 2021 and 2022. On July 1st, 2022 the total population stood at 10,698,973, making it the ninth most populous state in the U.S.

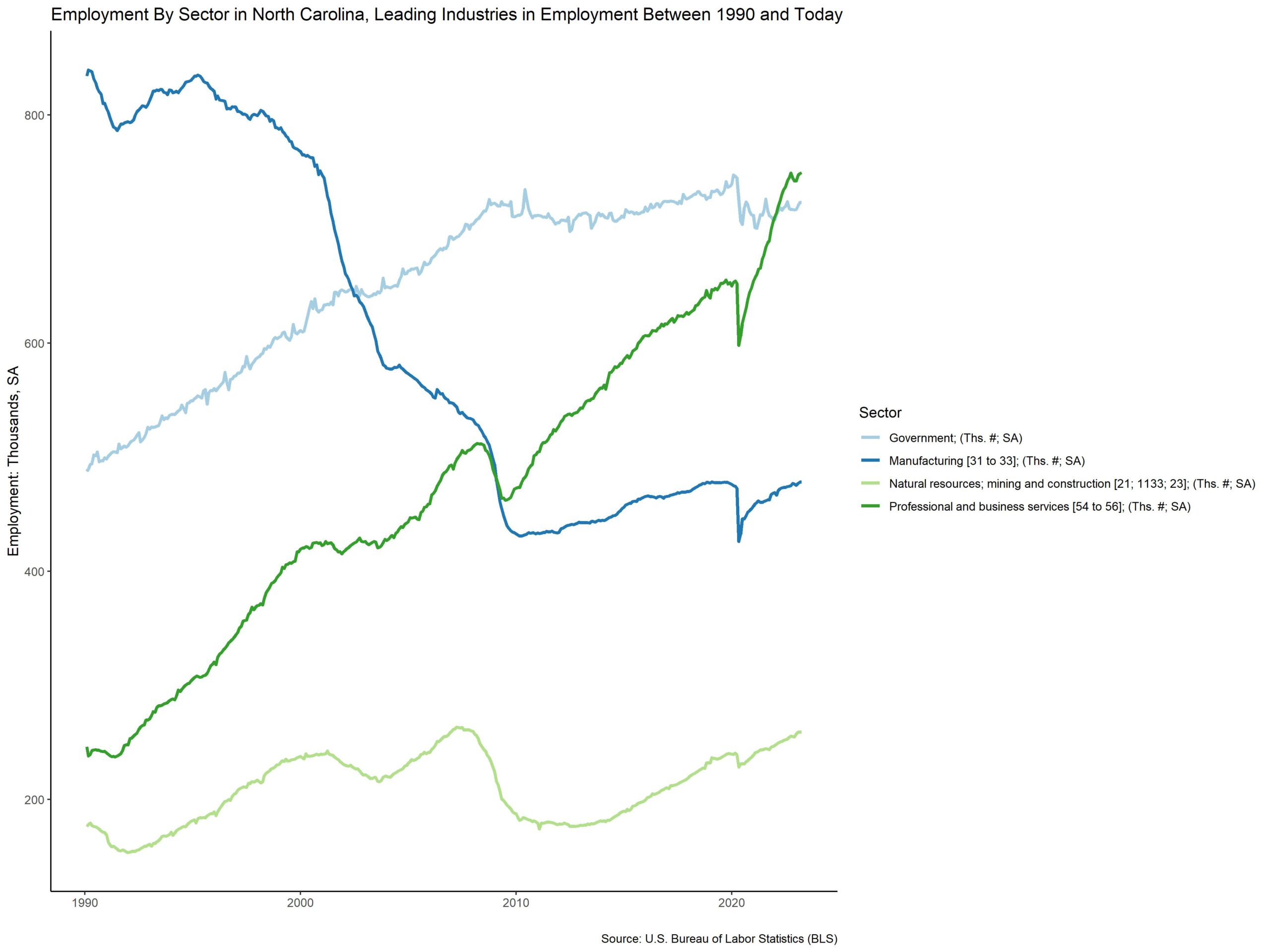

Over the past 30 years, like many states across the U.S., employment has shifted dramatically in North Carolina. Before 2003, the sector that employed the most North Carolinians was manufacturing. Manufacturing sector employment fell from approximately 830,000 workers in 1990 to 478,200 in March of this year, a 42.4% decrease. As of March 31st, 2023, the professional and business services sector is the largest employer in North Carolina, employing around 749,400 people. Only recently did this sector overtake the government sector as the largest employer in North Carolina. Government was the largest employer in North Carolina from May of 2003 to November of 2021. As of the end of March 2023, the government employed around 723,200 North Carolinians. The construction, mining, and logging industry ranks as the 8th largest employer in North Carolina, employing 259,000.

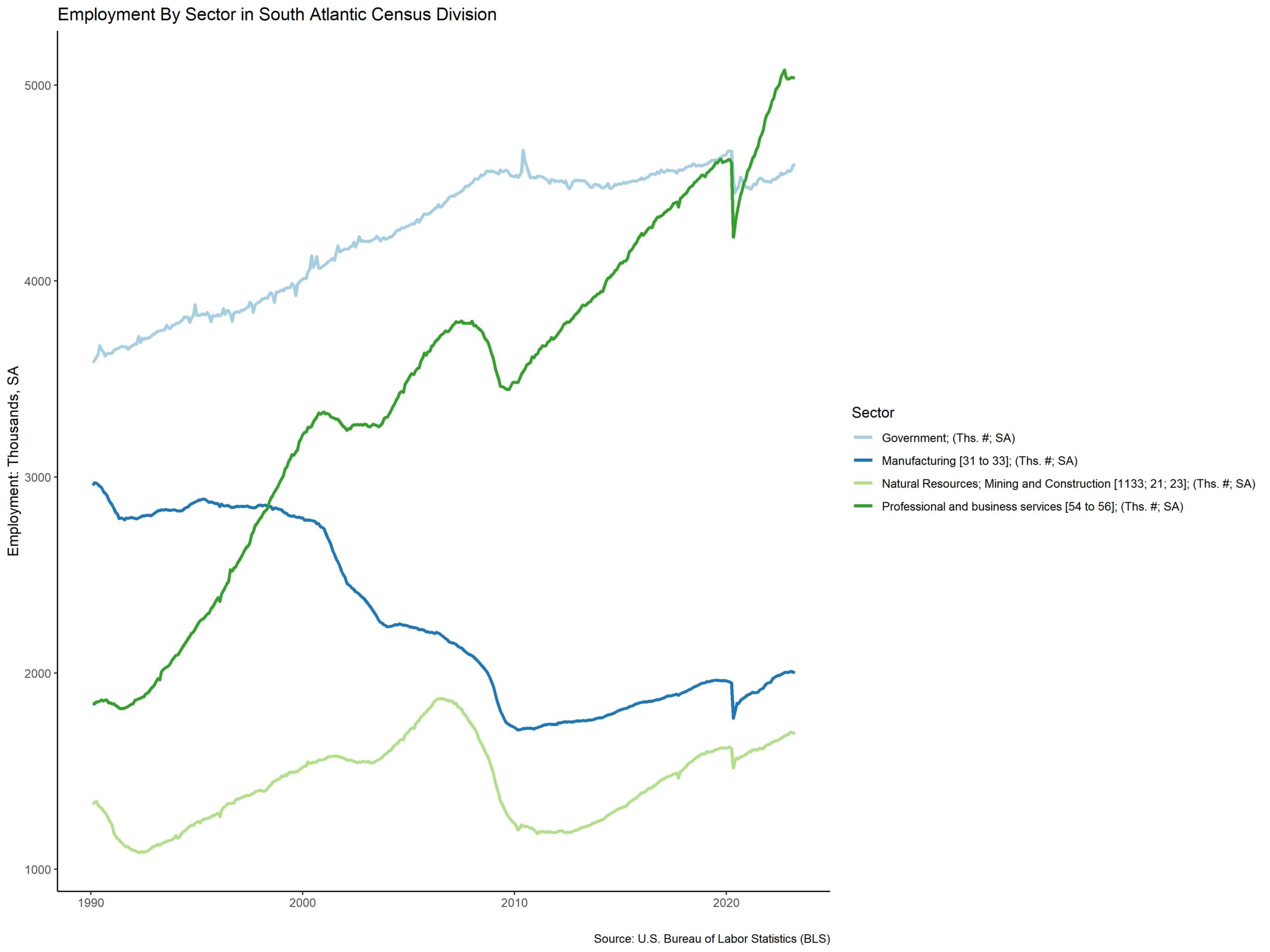

For comparison, the same employment sectors for the South Atlantic Census division, which includes D.C., DE, FL, GA, MD, NC, SC, VA and WV are displayed below. While manufacturing was never the leading employer in the South Atlantic, the number of people employed in this sector has fallen from around 3 million in 1990 to just below 2 million in 2023. The U.S. as a whole has lost around 5 million jobs in the manufacturing sector between 1990 and today due to automation and overseas competition. The professional and business services sector is the leading employer in the South Atlantic. This sector, similar to North Carolina, only recently became the largest regional employer as it overtook government employment in September of 2020. Government had been the leading employer for the previous 30 years.

Construction, mining and logging employs around 1.7 million persons in the South Atlantic region, employment in this sector still remains 200,000 employees below the 2006 pre-Great Recession high.

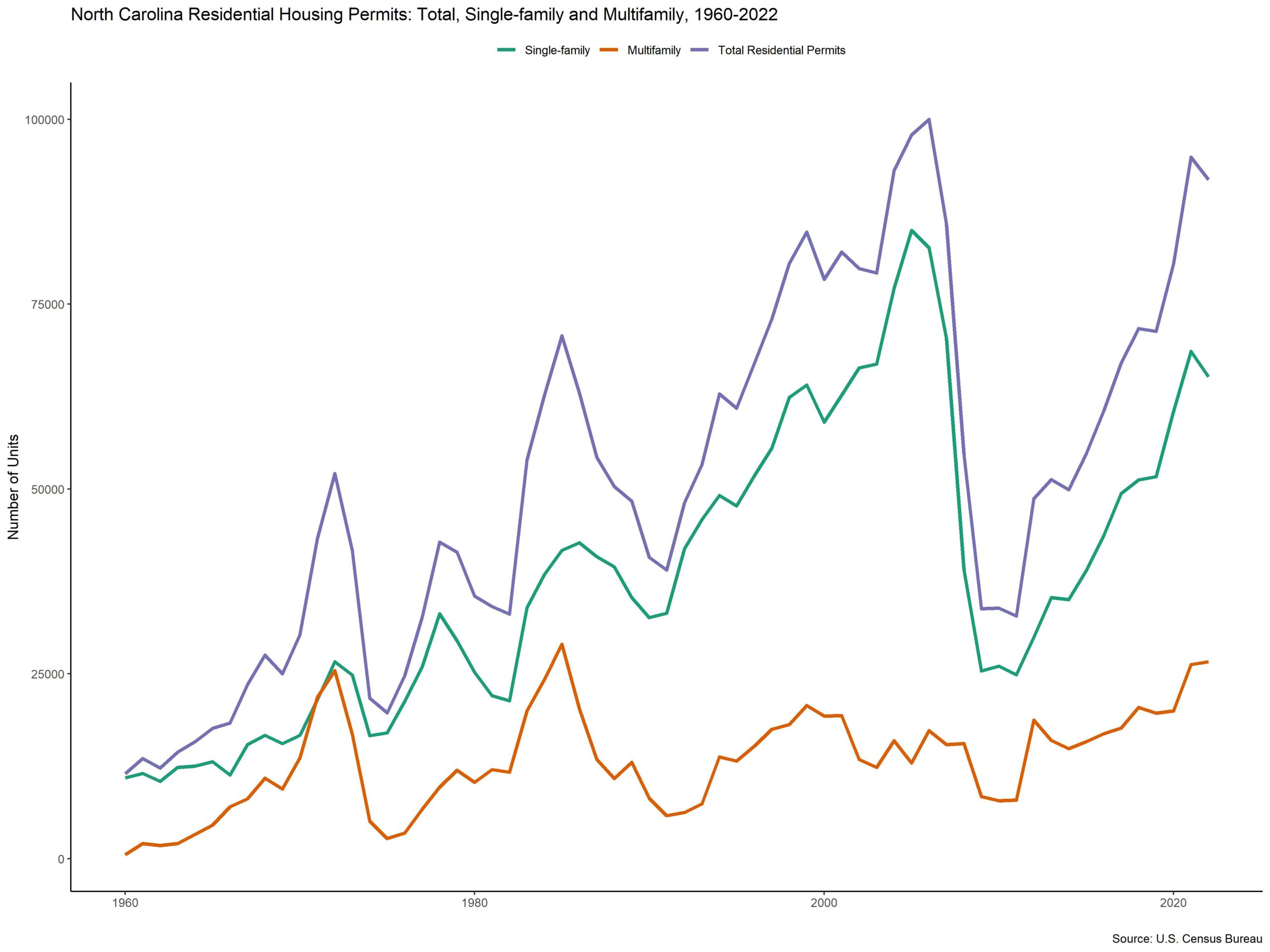

Based on annual Census permit data, the total number of single-family permits fell in 2022 while the total number of multifamily permits increased. For single-family permits in North Carolina, the state reached a peak at 84,975 total single-family permits in 2005. With the onset of the Great Recession, single-family permitting level fell to around 25,000 for 3 consecutive years from 2009 – 2011. Single-family permitting levels climbed for the next 10 years until this past year during which single-family permits experienced a decline. With multifamily permits, North Carolina reached a peak in 1985 at 29,004 permits. After 1985, multifamily permitting levels remained below 20,000 permits annually (except for 1999) for the next 23 years. Between 2018-2022, North Carolina multifamily permit levels have been above 20,000 for three of the past five years.

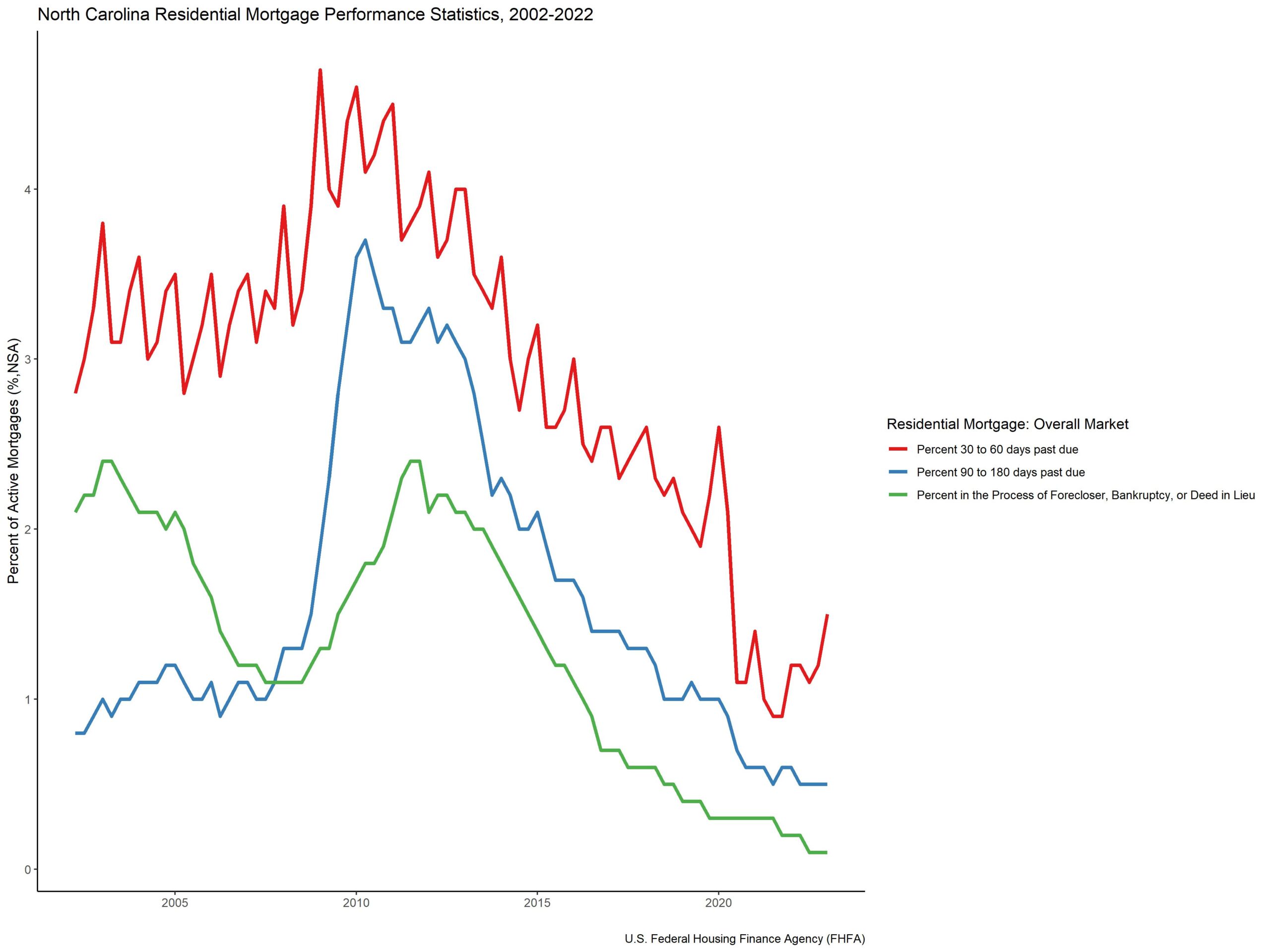

Data from the Federal Housing Finance Agency’s national mortgage database shows that the percent of residential mortgages 30-60 days late, 90-180 days late and in the process of foreclosure are much lower than pre-Great Recession levels. Staring with the percent of mortgages 30 to 60 days past due in North Carolina, pre-Great Recession levels were just above 3.0% of all mortgages in North Carolina. This share increased during the Great Recession and has fallen to levels below 1.5% in 2022. The percent of mortgages 30 to 60 days past due is more seasonal than any of the other series in the graph below, with the fourth quarter of a given year typically having a higher percentage than the first quarter of the same year. For 90 to 180 days past due in North Carolina, this percentage followed a similar trend. Pre-Great Recession levels were around 1.0%, this percent shot up to 3.7% in the first quarter of 2010. Over the next ten years, the percent of mortgages 90 to 180 days past due fell below 1.0% to 0.5% as of the third quarter of 2022.

The percent of mortgages in the process of foreclosure, bankruptcy, or deed in lien in North Carolina had been falling leading up to the Great Recession. This percentage was around 2.0% percent in 2002 and had fallen to 1.1% by 2008. The percentage went up to 2.4% by the third quarter of 2012, near where it was before 2005. Between 2012 and today, the percent of mortgages in the process of foreclosure fell to levels unseen since FHFA started reporting residential mortgages statistics in 2002. As of the third quarter of 2022, the percent is 0.1% of all mortgages in North Carolina.

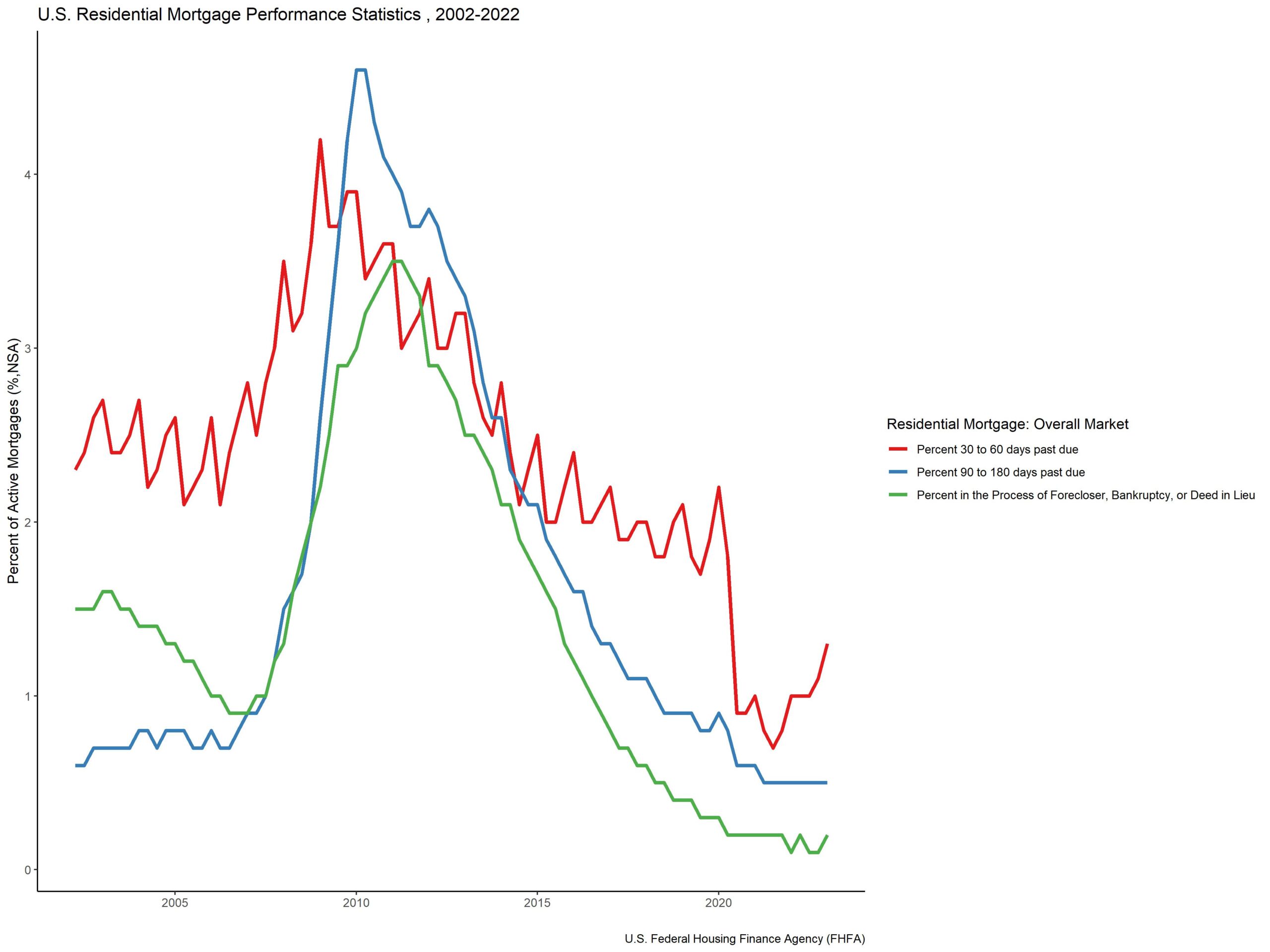

For comparison, below is the same set of statistics at the national level. The percent of residential mortgages that are 30 to 60 days past due has historically been at a lower level than North Carolina. Pre-Great Recession levels were between 0.3 – 1.1 percentage points lower than North Carolina; since the first quarter of 2018, this gap has never been more than 0.5 percentage points. For the percent of residential mortgages 90-180 days past due, U.S. levels post-Great Recession have been almost identical to that of North Carolina. During the Great Recessions, U.S. levels peaked at 4.6% between the third quarter of 2009 and the first quarter of 2010. This differs from North Carolina as its levels peaked at 3.7% in the first quarter of 2010. Another difference between the U.S. and North Carolina residential mortgages is that the percent of loans that were 90-180 days past due rose above the percent of loans 30-60 days past due for the U.S. This first occurred in the third quarter of 2009 and remained the trend for four consecutive years. In more recent years, both North Carolina and the U.S. have fallen to low levels for these mortgage statistics. The percent of mortgages in foreclosure, bankruptcy or deed in lien are both at historical lows being below 0.5% since late 2018.

Despite the population loss that North Carolina experienced in 2020, North Carolina continues to be one of the fastest growing states in the Union. It averaged the ninth fastest population growth since 2000 at 1.3%. Job growth has been strong since the Great Recession as North Carolina has seen job increases across the board. Construction jobs are almost back to pre-Great Recession levels and Business/Professional services has become the leading employer in the state. Manufacturing employment has even increased in recent years after falling to lows pre-Great Recession. Permit levels in North Carolina indicate that building will continue at higher rates for the coming years. Single-family permits have been above 50,000 for five consecutive years. The multifamily sector has also been building at historically elevated levels in North Carolina, being above 25,000 units per year over the past two years, having only previously been above 25,000 units permitted twice in the past 40-years. The mortgage market within North Carolina has been at historically low levels of late payments and foreclosures since the pandemic. Despite a recent uptick in the percent of active mortgages 30 to 60 days late, it remains well below another other point in the data series. The percent of active mortgages 90 to 180 days late is also at a historically low point in North Carolina, having been below 2.0% since the first quarter of 2015. The percent of active mortgages in foreclosure, bankruptcy or deed in lien has been below 0.5% of all mortgages since 2018, this trend mimics that of the national trend of a stronger mortgage market with far fewer foreclosures, bankruptcy or deed in lien since post-Great Recession. North Carolinas robust job growth, strong population growth and stable mortgage market conditions bode well for the future of the home building industry in North Carolina.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

With the increasing demand for housing, construction loans play a pivotal role in fueling the development of new residential projects that cater to the growing population. It’s encouraging to see how construction loans are instrumental in meeting the housing needs of a thriving state like North Carolina. Check us out at builderloans.net for your construction financing needs.

It’s fascinating to see how North Carolina’s population and employment landscape have evolved over the years, especially in light of recent challenges like the COVID-19 pandemic. Despite the setback in 2020, the state’s population has rebounded impressively, underscoring its resilience and attractiveness as a place to live and work.