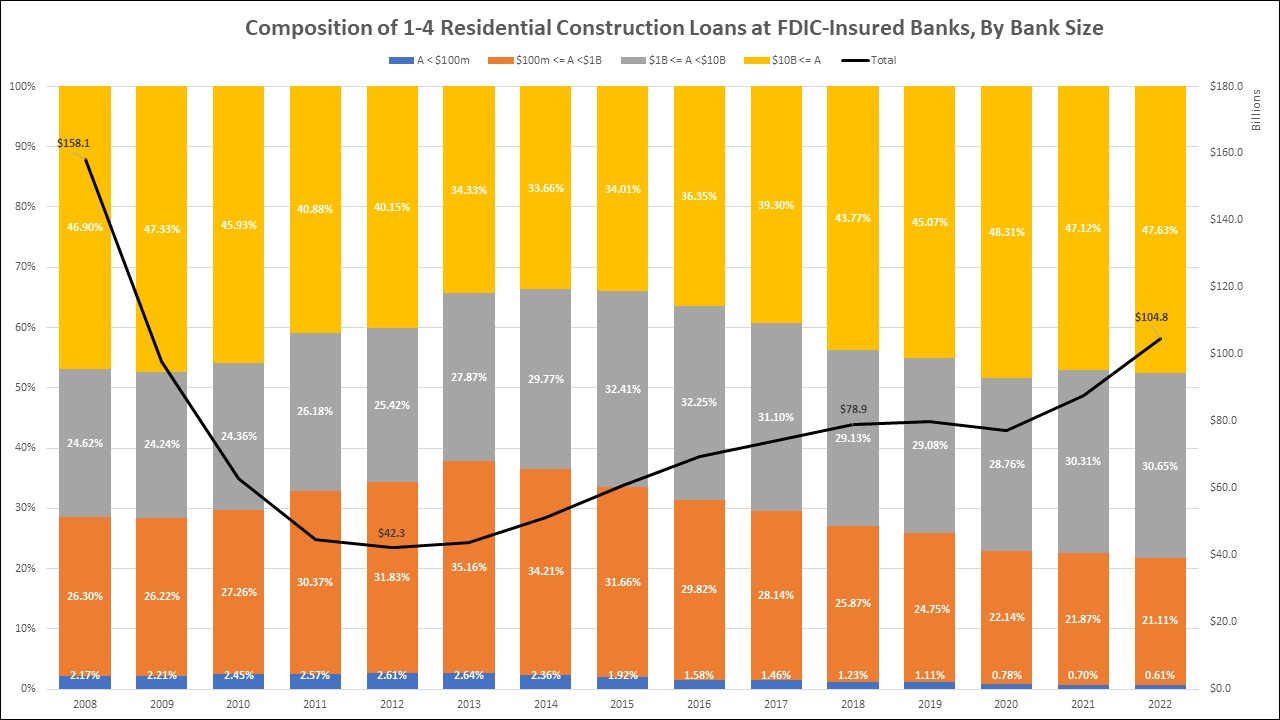

According to NAHB analysis of Federal Deposit Insurance Corporation (FDIC) data, large banks (assets greater than $10 billion) have increased their share of the residential construction loan market above pre-Great Recession levels in recent years. A 1-4 family residential construction loan is used for residential 1-4 family construction and land development. The majority of 1-4 residential construction loans are still held by small banks with less than $10 billion in assets, but their combined share of the residential construction market has decreased from 2014 highs.

The total balance of outstanding 1-4 residential construction loans was $104.8 billion at the end of 2022. The most recent AD&C analysis notes that this loan balance is increasing because newly built homes are remaining in inventory for longer as builders wait for buyers to return to the market. This balance has risen from a minimum of $42.3 billion over the past 10 years but remains much lower than the balance in 2008 ($158.1 billion). The share of residential construction loans has fluctuated as markets recovered and returned to normal following the Great Recession. Smaller banks (less than $10 billion in assets) held a 66.34% share of residential construction loans in 2014; this share fell to 52.37% in 2022.

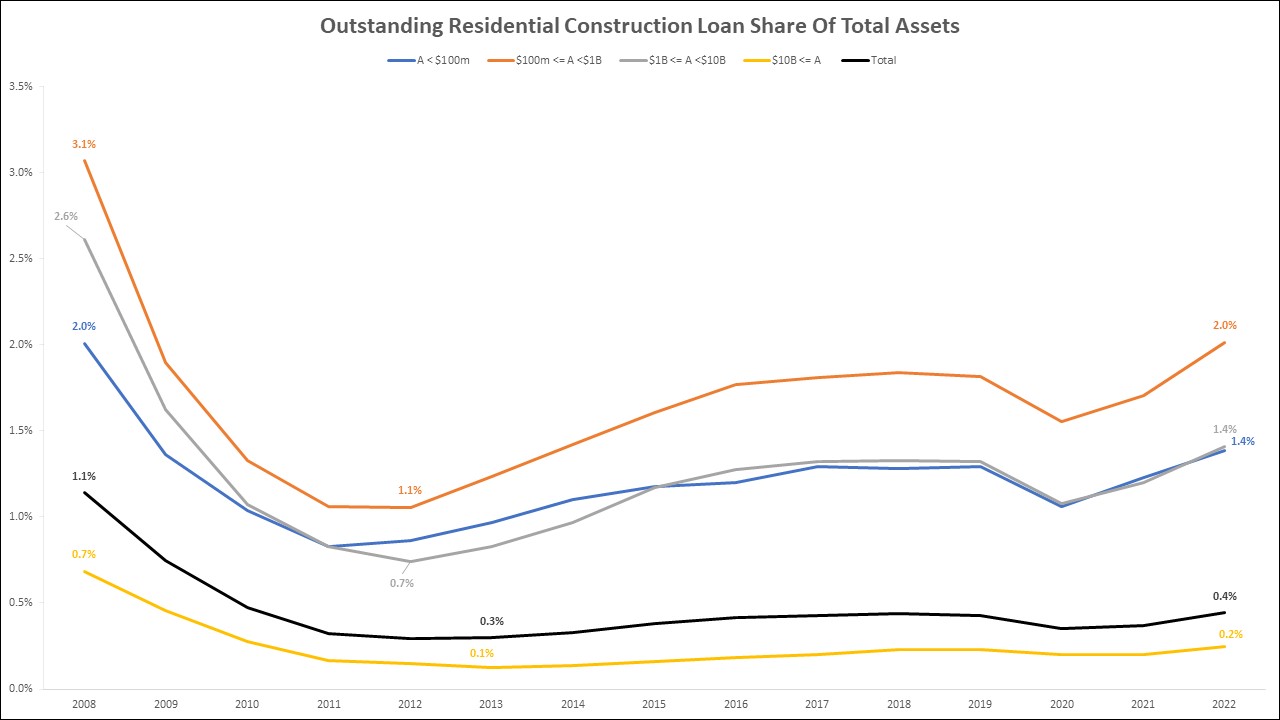

Scaling the residential construction loan balances by total assets, the largest banks have the lowest concentration of residential construction lending. Banks with more than $100 million in assets but less than $1 billion have the highest share of residential construction loans relative to total assets. By the end of 2022, the share of residential construction loan balance to total assets was 2.01% for banks with assets between $100 million and $1 billion — this is the highest ratio historically among all the bank sizes. Across all bank sizes, the share of residential construction loans to total assets continues to remain low relative to 2008.

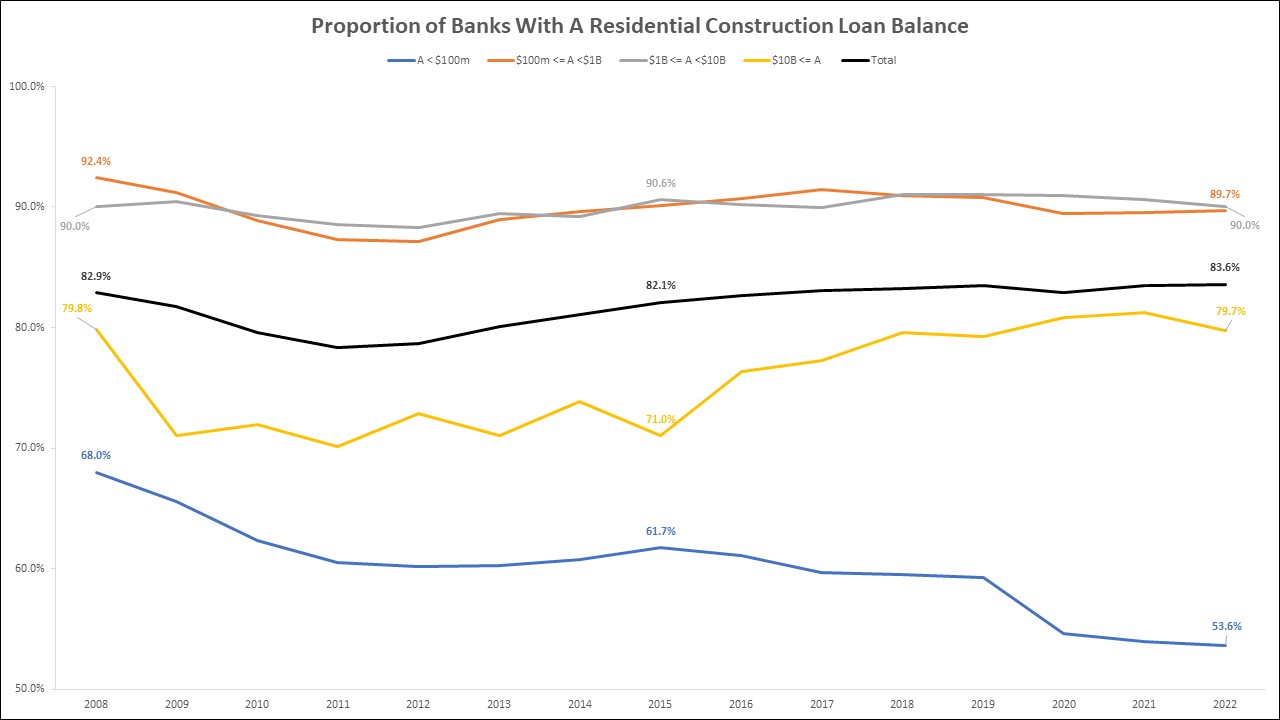

Another differentiation among the bank sizes is that historically, a significant majority of banks with assets between $100 million and $10 billion have held a 1–4 residential construction loan balance. Approximately nine out of ten banks with this asset size held a balance in 2022. For banks with more than $10 billion in assets, the share drops to around eight in ten. The smallest banks with assets less than $100 million have seen a continual drop in the share that hold residential construction loans. In 2008, 67.98% of banks with assets less than $100 million held a 1-4 residential construction loan balance; this share fell 14.37 percentage points to 53.61% by 2022. Across all banks, the proportion that have a residential construction loan balance reached a 14-year maximum at 83.57% in 2022.

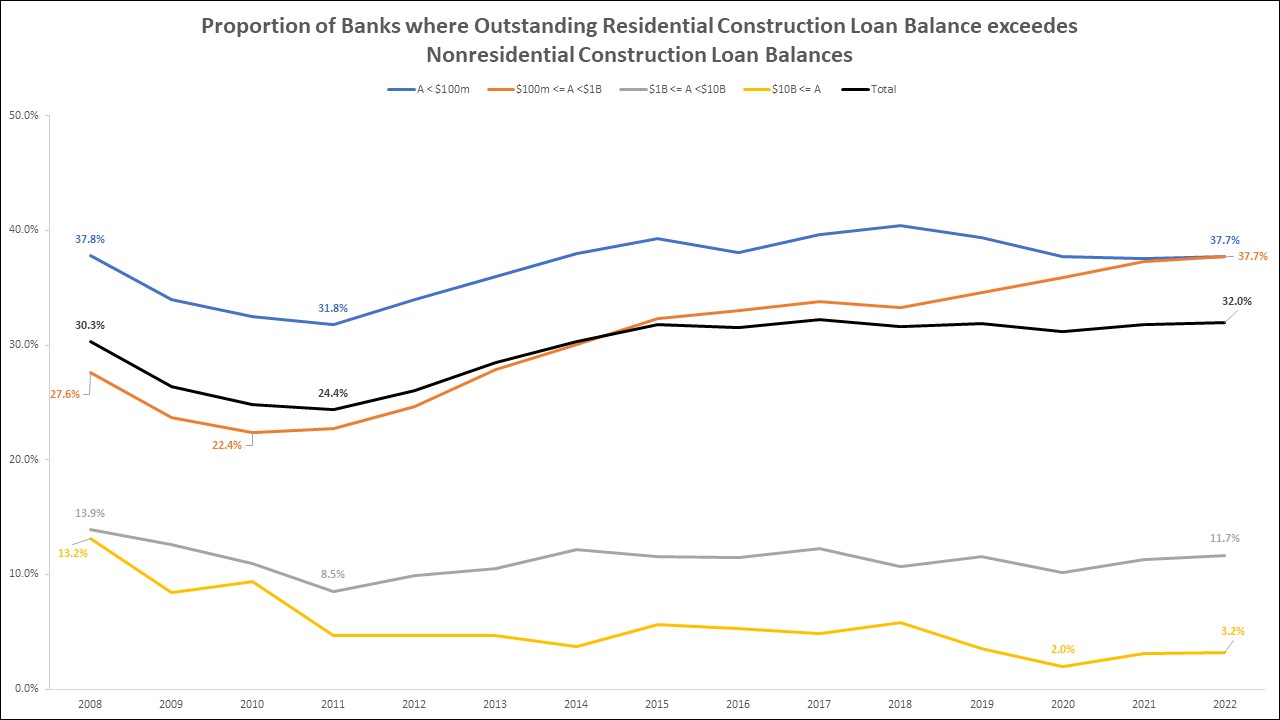

While only about half of banks with under $100 million in assets hold a 1-4 residential construction loan balance, the lowest of any bank size group, 37.71% of these small banks have an outstanding 1-4 residential construction loan balance that exceeds their nonresidential construction loan balance, the second largest proportion. In 2008, the proportion of banks with more than $100 million but less than $1 billion in assets that had a larger 1-4 residential construction loan balance than nonresidential construction was 27.57%. During the Great Recession, this proportion fell to 22.37% but has well surpassed the 2008 level by reaching 37.72% in 2022. For banks with assets between $1 billion and $10 billion, their proportion in 2022 was 11.66%, which is 2.24 percentage points lower than their 2008 level. The largest banks with more than $10 billion in assets had a proportion of 3.16% in 2022, well below their 2008 level of 13.16%.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

Very insightful! Check out builderloans.net to find out why and how we can get a clean and easy construction loan for you.