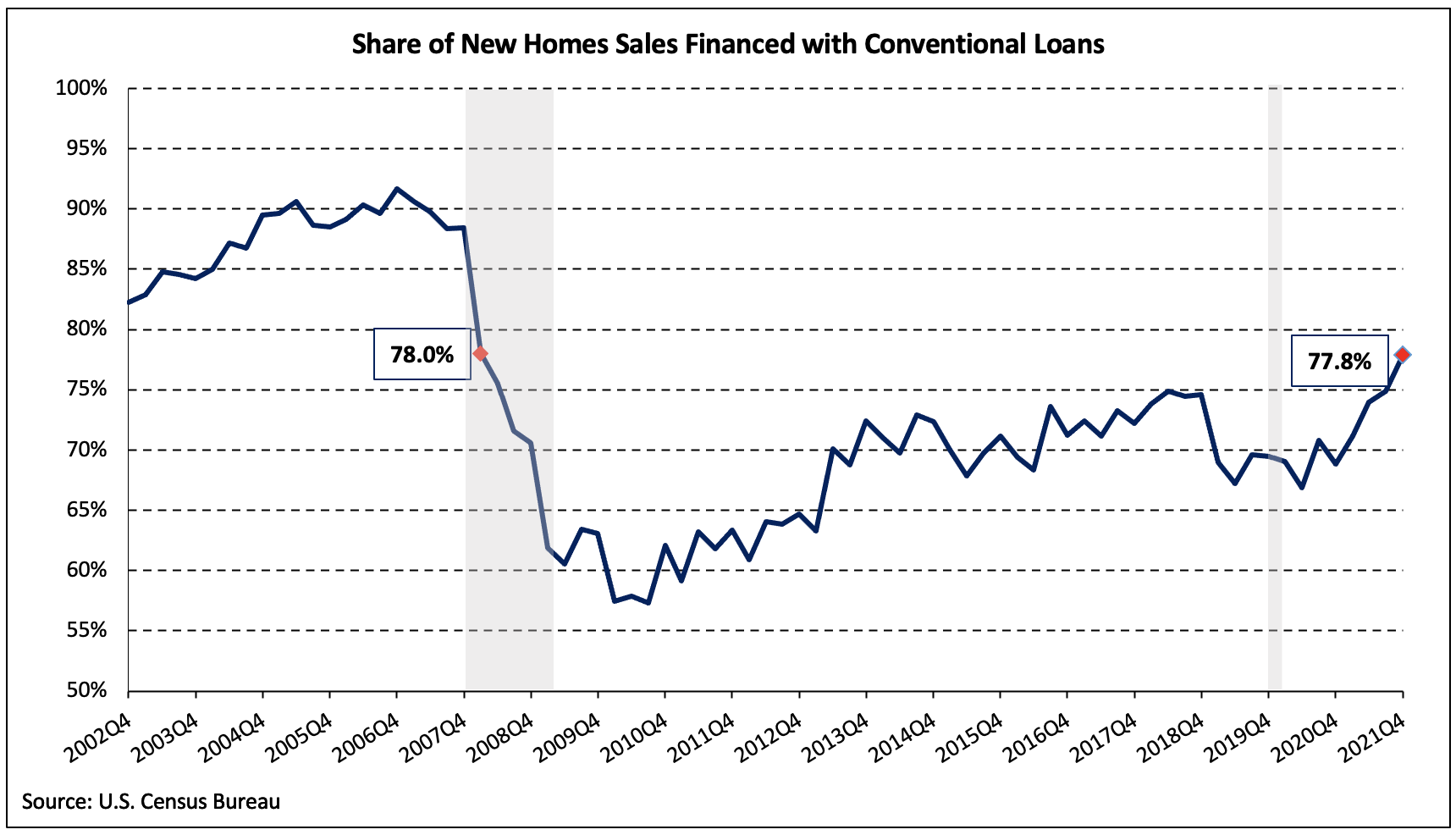

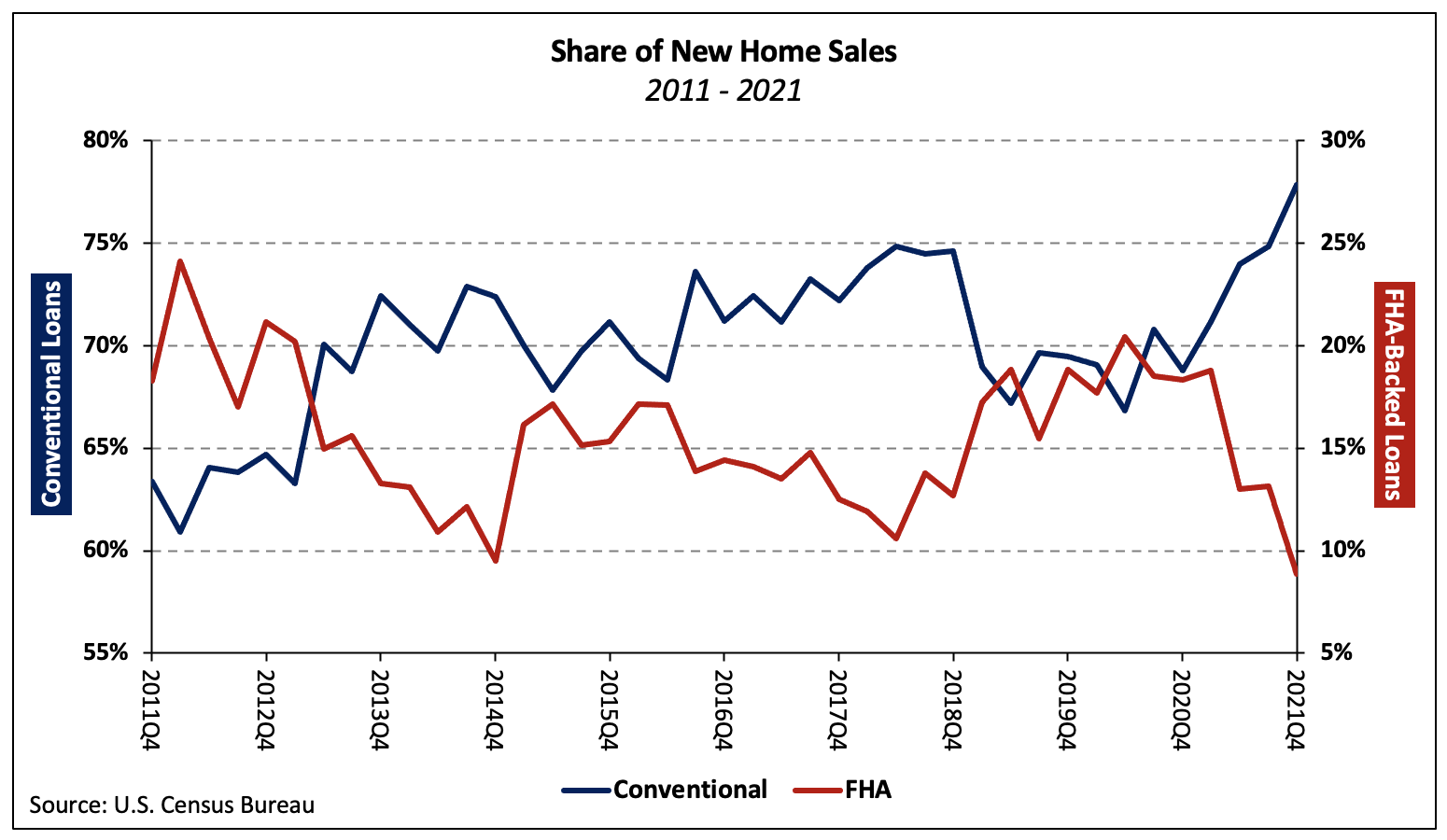

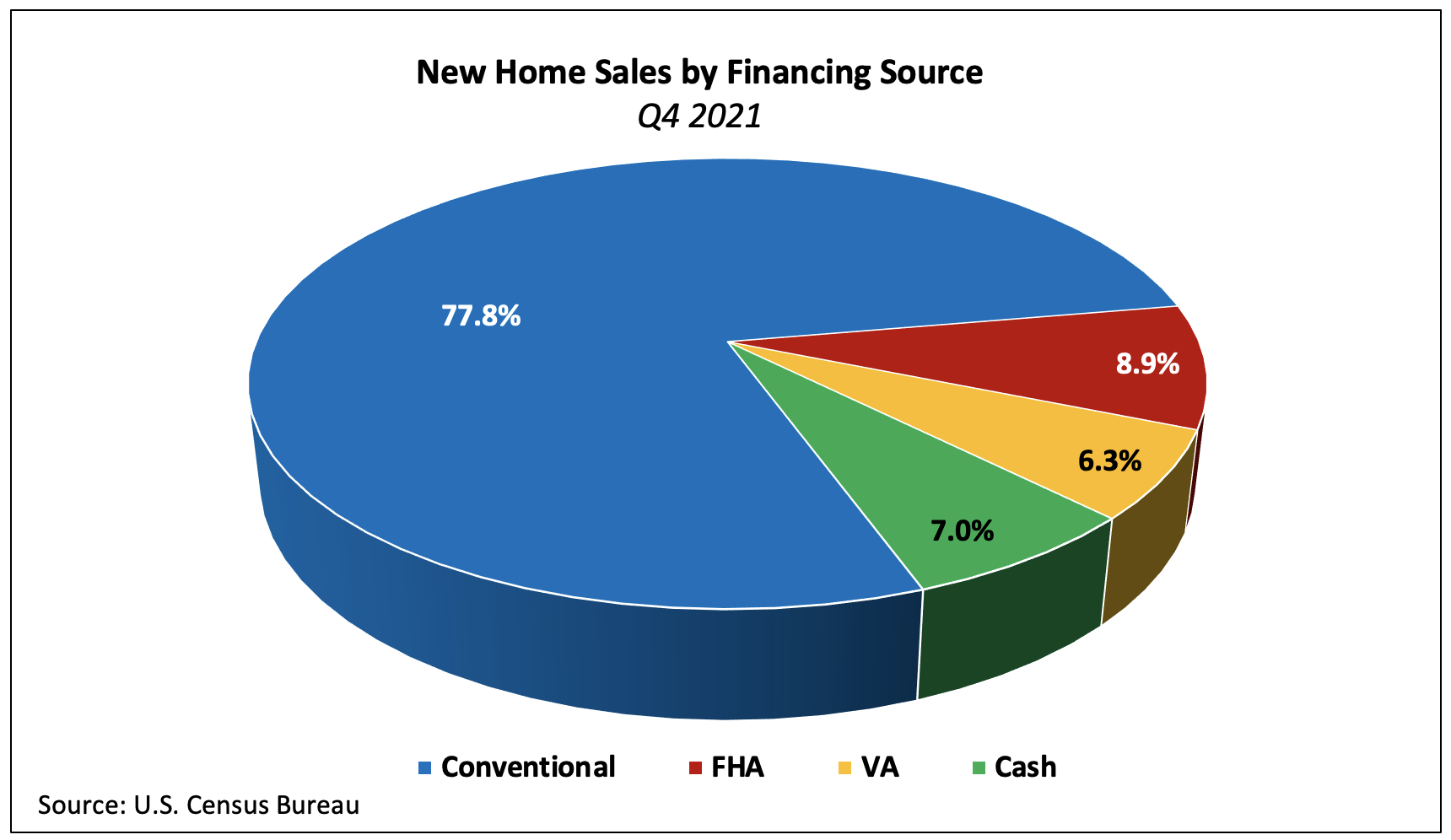

NAHB analysis of the most recent Quarterly Sales by Price and Financing published by the U.S. Census Bureau reveals that conventional loans financed 77.8% of new home sales in the fourth quarter of 2021—the largest share since Q1 2008. The share increased 2.9 percentage points over Q3 2021 (revised) and has risen each of the last four quarters, up 9.0 percentage points since Q4 2020.

Conversely, the FHA-backed share of new home sales fell to 8.9% in the fourth quarter—a 4.2 percentage point decline (quarter-over-quarter) and 9.4 percentage points lower than the Q4 2020 share. The four-quarter moving average (MA) of the share of new home sales financed through FHA was 13.4%–the lowest it has been since Q4 2018.

As conventional loan market share increases, the FHA share typically falls and vice versa. Over the past four quarters, the share of new home sales (four-quarter moving average) financed with conventional loans has climbed 5.6 ppts while FHA’s market share has decreased 5.3 ppts.

The share of VA-backed sales increased to 6.3% in the fourth quarter but is 1.1 ppts lower than the share one year prior. Cash purchases made up a slightly higher share of sales in the fourth quarter—up 0.1 ppt—as they accounted for 7.0% of the total.

The share of cash purchases has climbed each of the past three quarters since reaching its most recent trough of 4.4% and is the largest share since Q4 2014. The reported number of cash sales declined 1,000, or 8.5%, in the fourth quarter but increased by 1,000 on a year-over-year basis.

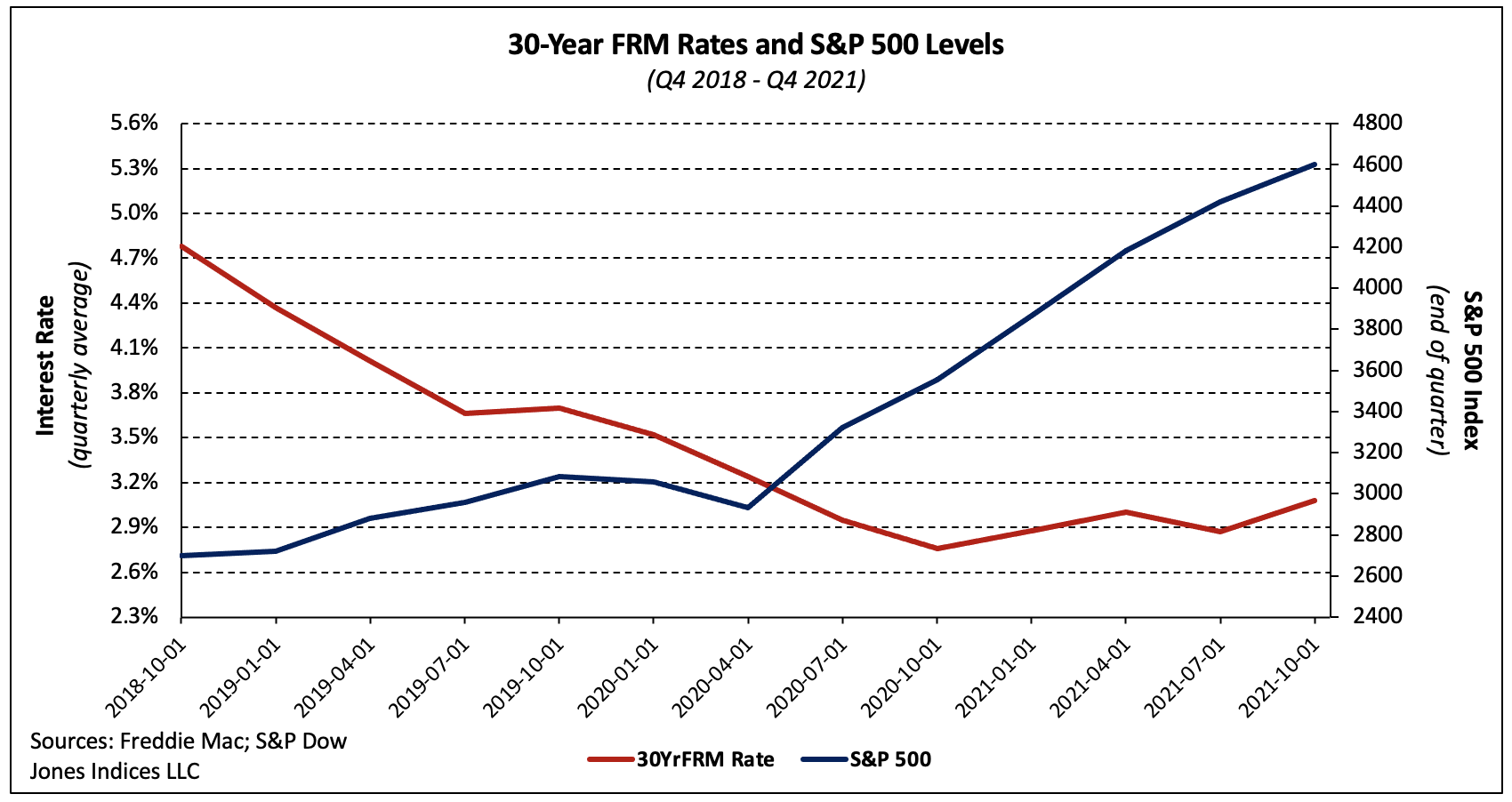

The average interest rate of a 30-year fixed rate mortgage increased 21 basis points, quarter-over-quarter—to its highest quarterly average since Q2 2020. Stock market returns (proxied by the S&P 500®) in the fourth quarter were 4.1%, quarter-over-quarter, and 29.5% year-over-year.

Each of factors has played an important role in the large increase in the share of conventional loan and cash purchases relative to sales financed through the FHA and VA. Higher stock returns and the resulting increased wealth aids borrowers in the underwriting process as well as increasing the down payment a household can afford (should they cash out some of their portfolio).

Low mortgage rates improve the odds that a given loan will be approved, all else held equal, as they keep monthly payments lower than they would otherwise be. As the monthly payment for a loan of a certain amount decreases, it becomes less likely that the future payments would increase the borrower’s debt-to-income ratio above a financial institution’s risk threshold.

Although cash sales make up a small portion of new home sales, they constitute a larger share of existing home sales. According to estimates from the National Association of Realtors, 23% of existing home transactions were all-cash sales in December 2021, down from 24.0% in November 2021 and up from 19.0% in December 2020.

Different sources of financing also serve distinct market segments, which is revealed in part by the median new home price associated with each. In the fourth quarter, the national median sales price of a new home was $408,100. Split by types of financing, the median prices of new homes financed with conventional loans, FHA loans, VA loans, and cash were $442,300, $315,100, $373,900, and $359,400, respectively.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.