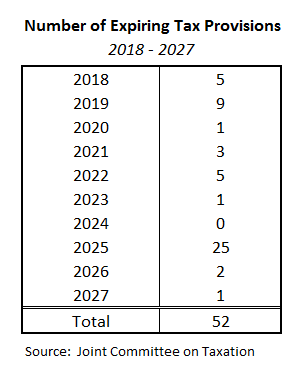

The Tax Cuts and Jobs Act (TCJA) added numerous temporary provisions to the tax code. Temporary tax law can be difficult to track and compliance can be expensive. Earlier this year, the Joint Committee on Taxation released a guide to expiring tax provisions, sorted by year of expiration. The table below shows how many items in the tax code will expire each year through 2027.

Although most corporate tax provisions were made permanent in TCJA, that left tax cuts benefitting individuals and pass-thru businesses on the chopping block. If these provisions are left unaddressed prior to current expiration dates, the country will face a situation similar to 2012’s “fiscal cliff” when December 31st, 2025 rolls around.

At that point, 23 provisions from TCJA relating to individual income taxes are set to expire.

As most home builders are organized as pass-thru entities (i.e. LLCs, LLPs, S-corps), perhaps the most important provision in this tranche of expiring provisions is the 20 percent deduction for pass-thru income. The deduction provides for a deduction up to 20 percent of an individual’s “qualified business income.”

Directly tied to the benefits of that deduction are individual income tax rates, all of which were lowered in TCJA. Without any changes, tax rates would revert to their pre-reform levels. In isolation, expiration of the business income deduction and individual tax rate reductions would raise taxes on business owners. The effects would be exacerbated if both expire as scheduled. In that case not only would taxpayers pay higher income tax rates, but more of their income would become taxable.

In addition, the Alternative Minimum Tax (AMT) exemption and phaseout threshold would return to prior law. The TCJA made the AMT far less burdensome, reducing AMT-payers from over five million to roughly 200,000.

The increased standard deduction, child tax credit, and estate tax exemption are also set to expire at the end of 2025.

On the flip side, multiple provisions of TCJA that made homeownership more expensive will revert back to prior law in 2026. If the law is not changed by then:

1. The cap on the mortgage interest deduction will go back to $1 million (currently $750,000).

2. The new $10,000 cap on deductions for state and local income and property taxes will be eliminated.

3. The specific $100,000 deduction for interest on home equity lines of credit (HELOCs) will be available once again.

It is worth noting that, even if the individual income tax code returns to its pre-TCJA form, inflation adjustments will continue to be determined by the chained consumer price index (C-CPI). This would result in most taxes increasing when compared to their pre-TCJA levels.

Beginning at the end of 2022, “full expensing” (i.e. 100 percent first-year depreciation) will begin to phase out. After December 31st, 2022, the deduction percentage will decrease by 20 percent yearly, until it completely expires in the end of 2026.

These are just a few tax provisions set to expire over the next decade. Some may be extended or made permanent, while at least some of them will likely expire as scheduled. It is important that taxpayers closely follow the debate as it plays out so they can plan for smooth transitions between changes made to the code.

DISCLAIMER

This article is for informational purposes only. It should not be considered tax advice. Before making any tax decisions, work with a tax professional. For more detail, please see the full disclaimer.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.