Ever since the inception of the U.S. income tax in 1913, home owners have been able to deduct interest paid on home equity loans (HELOCs). The Omnibus Budget Reconciliation Act of 1987 limited the mortgage interest and HELOC deductions to interest paid on $1,000,000 and $100,000 of debt, respectively. Then came the Tax Cuts and Jobs Act of 2017 (TCJA).

The TCJA included the first major changes to these interest deductions in 30 years. Although the headline housing change was the $750,000 cap placed on the mortgage interest deduction (MID), the law also eliminated the deduction for interest paid on HELOCs—a potentially significant cut to the remodeling industry.

After combing through prior law and regulatory guidance regarding HELOC debt, NAHB came to the conclusion that interest paid on home equity loan debt remains deductible under the new law. The $100,000 limit specific to HELOCs had been removed, but NAHB felt that indebtedness secured by a taxpayer’s residence fell under the definition of “acquisition debt” and should be considered “qualified mortgage interest.”

Three weeks after submitting a letter to Treasury Secretary Steven Mnuchin that laid out our concerns, the Internal Revenue Service issued guidance agreeing with our assessment:

“[D]espite newly-enacted restrictions on home mortgages, taxpayers can often still deduct interest on a home equity loan, home equity line of credit (HELOC) or second mortgage, regardless of how the loan is labelled….Under the new law, for example, interest on a home equity loan used to build an addition to an existing home is typically deductible…As under prior law, the loan must be secured by the taxpayer’s main home or second home (known as a qualified residence), not exceed the cost of the home and meet other requirements.”

The main “other requirement” is that interest paid may only be fully deducted if the combined mortgage and HELOC loan balances of the taxpayer do not exceed $750,000. If, for example, a taxpayer borrowed $200,000 to build an addition to their home but also still owed $600,000 on the original mortgage, their total debt is $800,000–$50,000 over the limit. Therefore, their deduction is limited to the amount of interest they paid reduced by 6.25% ($50,000 over the limit, divided by $750,000).

In 2016, the most recent year for which data is available, home owners owed $280.4 billion on all HELOC debt and $89.7 billion on HELOCs used for home improvement (HI). As only taxpayers who itemize receive a tax benefit from the HELOC deduction, this is the group of potential customers whose decisions to remodel their home are influenced by interest deductibility.

Of the $89.7 billion in outstanding HI HELOC balances, $76.2 billion (85.0%) was owed by families that itemized their tax returns. In addition, because the limit has been reduced from $1 million to $750,000, only the portion of loans under this cap are applicable to the analysis. Fortunately, the vast majority of HI loans—$70.5 billion worth, or 92.5% by outstanding balance—still qualify for the interest deduction.

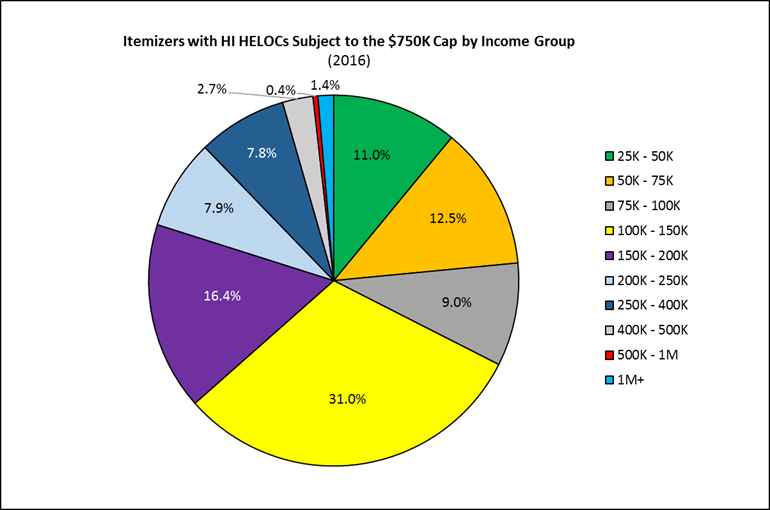

More than 1.3 million itemizers made $2.8 billion of interest payments on HI HELOCs in 2016—25.4 percent of interest paid on all HELOC debt. While borrowers span the income spectrum (below), majority of these taxpayers made between $75,000 and $200,000.

Source: Federal Reserve, 2016 Survey of Consumer Finances; NAHB calculations

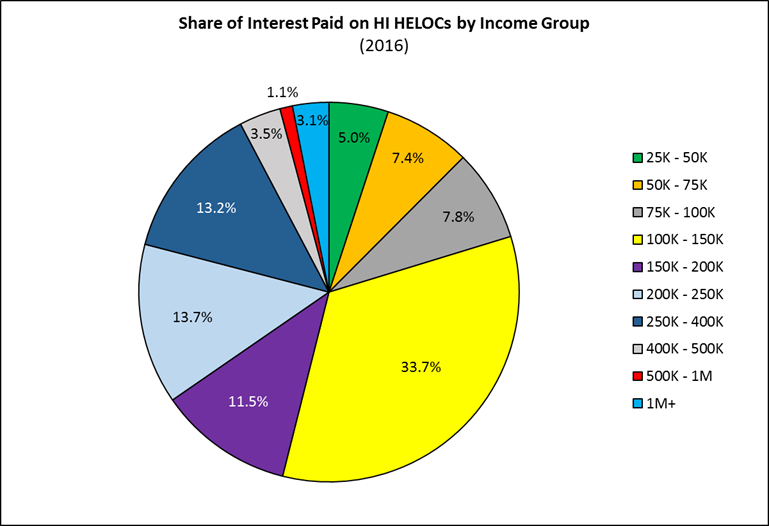

The distribution of interest paid on home improvement HELOCs is similar, but leans toward upper income earners as the outstanding balance on loans tends to increase with income, on average.

Source: Federal Reserve, 2016 Survey of Consumer Finances; NAHB calculations

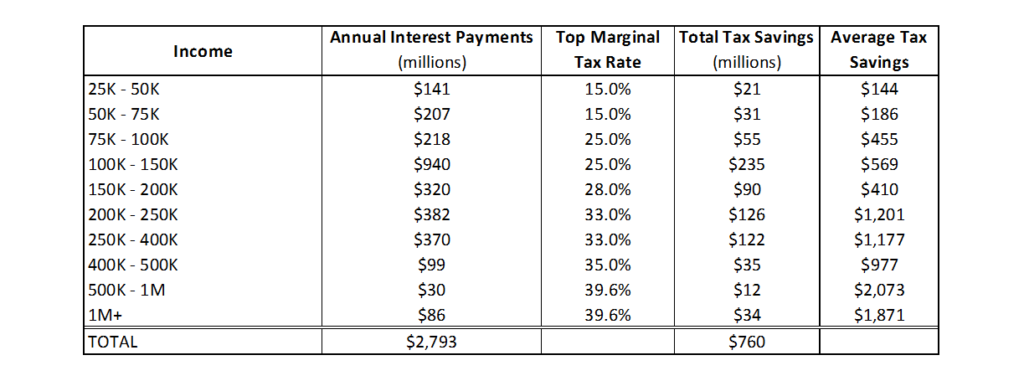

The tax savings due to the retention of the HELOC interest deduction for purposes of substantially improving a home are calculated by multiplying deductible interest by the applicable top marginal tax rate for each income group. The table below shows total as well as average tax savings per income group that is attributable to the deduction for home equity debt interest.

Source: Internal Revenue Service; Federal Reserve, 2016 Survey of Consumer Finances; NAHB calculations

The $760 million in tax savings represents the dollar value of remodeling incentives that was retained when the IRS publicly agreed with NAHB’s analysis.

The new tax law made two major changes to the individual tax code that will affect this amount in future years.

First, the TCJA doubled the standard deduction available to taxpayers. As a result, the Joint Committee on Taxation (JCT) estimates that the percentage of taxpayers who itemize will decline from 31% in 2017 to 13 percent—or 20.4 million—in 2018. This reduction in itemizers means that fewer home owners are likely to take the HELOC interest deduction into account when making a renovation decision.

Offsetting this reduction, however, is the increase in itemizers who may claim the deduction as a result of changes to the alternative minimum tax (AMT). Families forced to pay the AMT are not permitted to deduct interest on a HELOC loan from their taxable income. In 2017, more than 5 million taxpayers—97.4 percent of which earned more than $100,000—owed AMT.

The new tax law increased the income threshold for the AMT to $1 million. Accordingly, JCT estimates that only 600,000 taxpayers will pay the AMT in 2018. The reduction in demand caused by the increase in the standard deduction should be offset, at least partially, by these additional 5 million taxpayers who can now offset their tax liability with interest payments on HELOC loans.

The demographics of these new potential customers will also work to increase demand. More than 95 percent of taxpayers who paid the AMT in 2015 (the most recent year for which IRS data available) made between $100,000 and $1 million. Over three-quarters of outstanding HI HELOC debt is owed by borrowers in this income range.

As NAHB stated in its letter to Sec. Mnuchin, HELOC loans are “the lifeblood of the remodeling industry.” The elimination of the deduction for HELOC interest payments would have taken a major financing tool away from families that want to substantially improve their home so they can remain in the neighborhood they love or age in place. With the deduction resurrected, remodelers’ customers will have hundreds of millions worth of tax benefits incentivizing them to renovate their home.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.