Lending standards were essentially unchanged1 for all residential mortgage categories in the third quarter of 2024, except for Subprime loans, according to the Federal Reserve Board’s October 2024 Senior Loan Officer Opinion Survey (SLOOS). Demand for most residential mortgage loans remained weaker across all categories in the quarter. Lending conditions for commercial real estate (CRE) loans were moderately tight, amid modestly weak demand as well. However, NAHB believes that financial conditions for the home building industry should improve next year as the Federal Reserve continues along their current rate cutting cycle.

Residential Mortgages

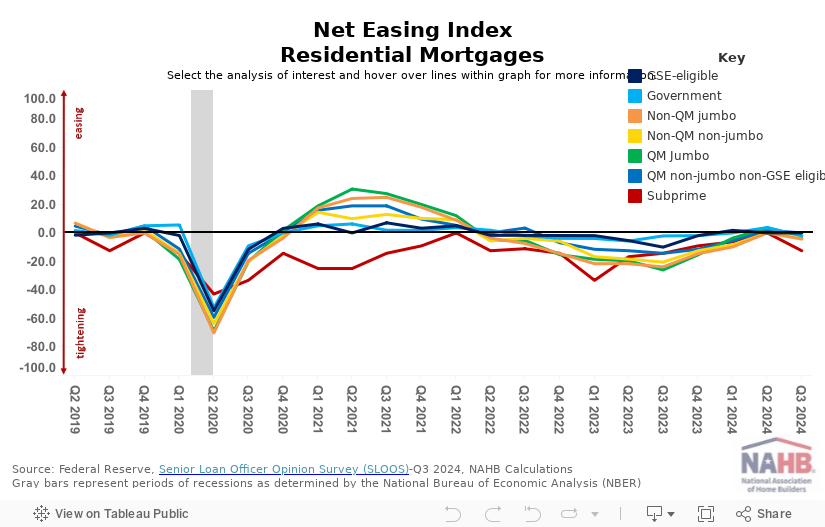

GSE-eligible and Qualified Mortgage (QM) non-jumbo non-GSE eligible mortgages recorded a neutral net easing index2 value (i.e., 0) while the other five residential mortgage loan types (Subprime, Non-QM jumbo, QM jumbo, Non-QM non-jumbo, Government) were negative for the third quarter of 2024, representing tightening conditions.

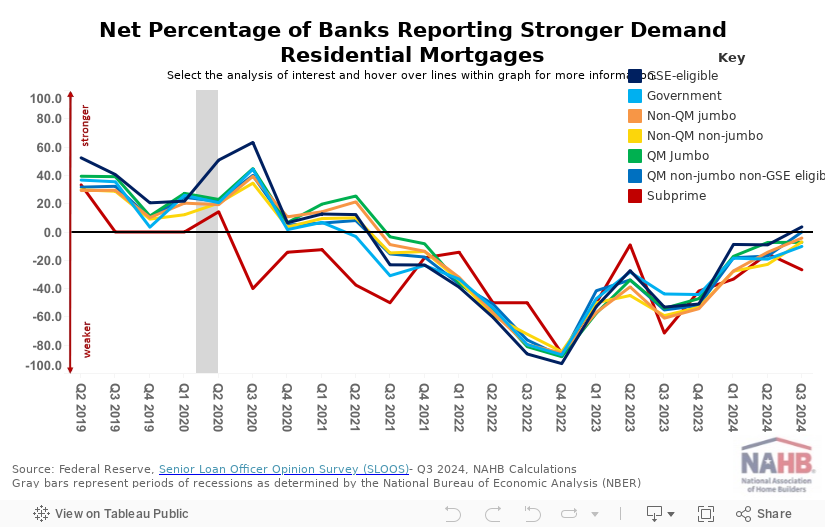

Besides GSE-eligible, which posted stronger demand (i.e., positive value) for the first time since Q2 2021, and QM non-jumbo non-GSE eligible (neutral demand), all other residential mortgage loan categories reported weaker demand in Q3 2024. Weakness is less widespread than in recent quarters, however. Among all residential mortgage loan categories, falling demand is best highlighted by Subprime loans which experienced weaker demand for 17 consecutive quarters, or for over four years.

Commercial Real Estate (CRE) Loans

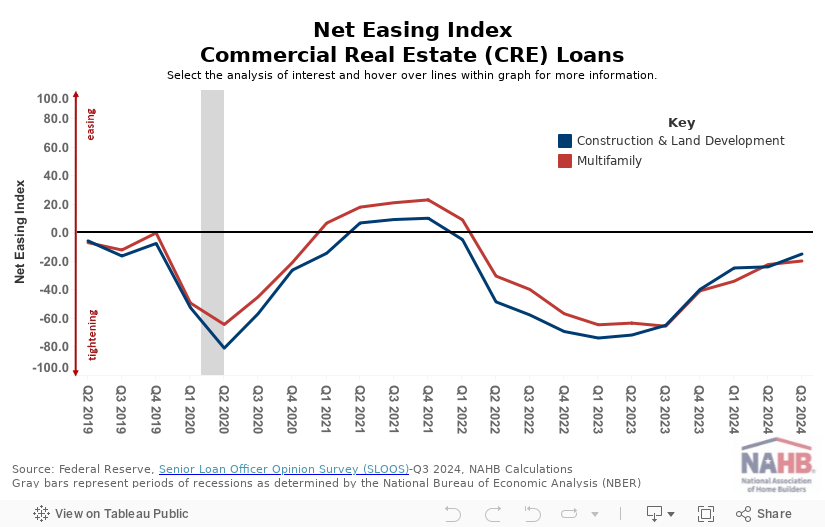

Banks reported moderately tightening lending conditions for both multifamily as well as all CRE construction & development loans in the third quarter of 2024. However, the tightening was not as widespread as in recent quarters. Results show 10 consecutive quarters of tightening lending conditions for CRE loans.

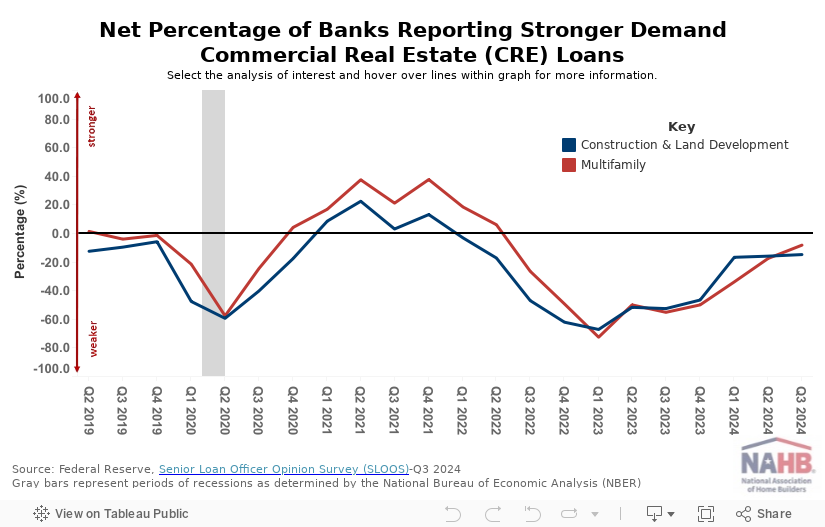

For multifamily, the net percentage of banks reporting stronger demand was -8.2% while –14.8% for construction & development loans. Although improving, weaker demand has continued for over two years for both CRE loan categories.

- The Federal Reserve uses the following descriptors when analyzing results from the survey which will be used, in principle, within this blog post as well:

– “Remained basically unchanged” means that the change or actual reading is greater than or equal to 0 and less than or equal to 5 percent.

– “Modest” means that the change or actual reading is greater than 5 and less than or equal to 10 percent.

– “Moderate” means that the change or actual reading is greater than 10 and less than or equal to 20 percent.

– “Significant” means that the change or actual reading is greater than 20 and less than or equal to 50 percent.

– “Major” means that the change or actual reading is greater than or equal to 50 percent. - A value above zero (i.e., positive) indicates that lending conditions are easing while a value below zero (i.e., negative) indicates that lending conditions are tightening.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.