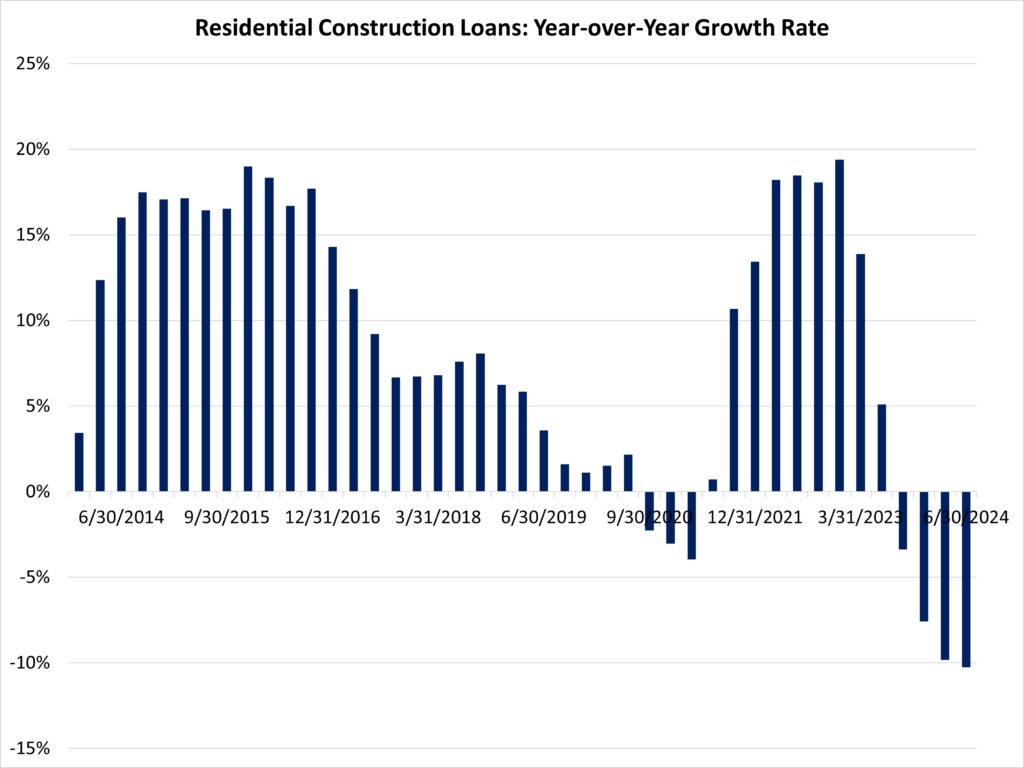

During the second quarter of 2024, the volume of total outstanding acquisition, development and construction (AD&C) loans posted the largest year-over-year percentage decline since 2012, as interest rates remain elevated before the beginning of the Fed cutting short-term interest rates in September. AD&C loan conditions will improve as the Fed progresses in its policy easing cycle.

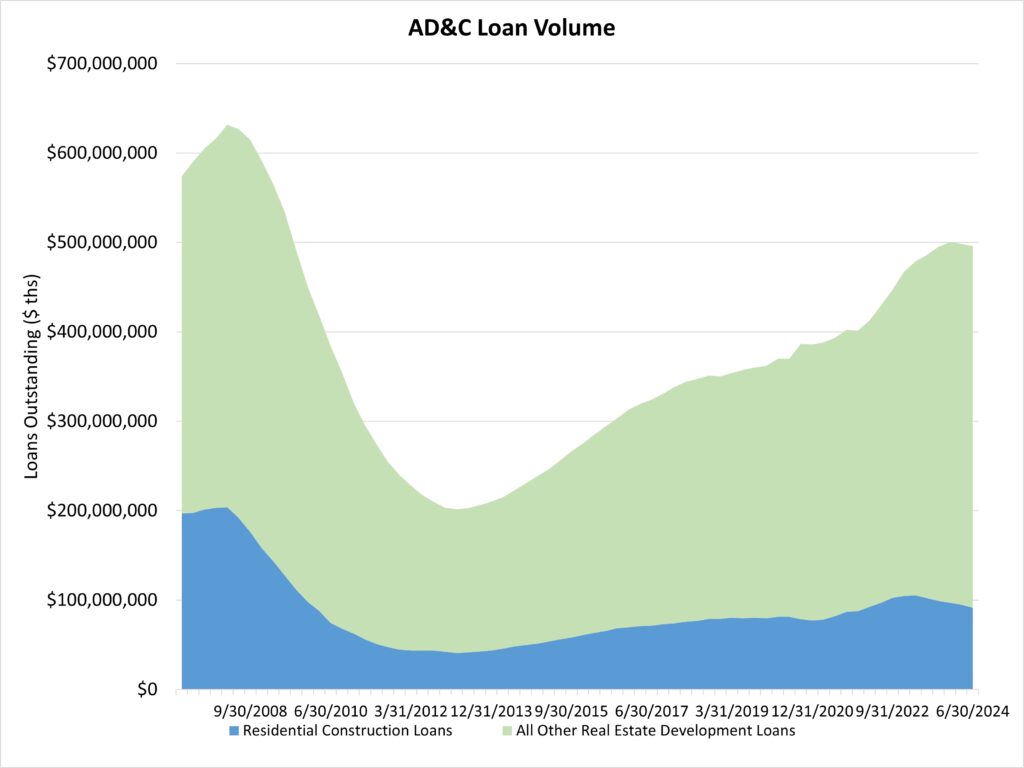

The volume of 1-4 unit residential construction loans made by FDIC-insured institutions declined 3.5% during the second quarter. The outstanding stock of loans declined by $3.3 billion for the quarter. This loan volume retreat places the total stock of home building construction loans at $92 billion, off a post-Great Recession high set during the first quarter of 2023 ($105 billion). The decline in loan volume is holding back private builder home construction and acting as a limiting factor for home builder sentiment.

On a year-over-year basis, the stock of residential construction loans is down more than 10%, the largest year-over-year decline since 2012. This contraction for construction financing is a key reason home builder sentiment moved lower at the end of 2023, even as building activity accelerated, propelled by larger builder activity.

It is worth noting the FDIC data represent only the stock of loans, not changes in the underlying flows, so it is an imperfect data source. Lending remains much reduced from years past. The current amount of existing residential AD&C loans now stands 55% lower than the peak level of residential construction lending of $204 billion reached during the first quarter of 2008. Alternative sources of financing, including equity partners, have supplemented this capital market in recent years.

The FDIC data reveal that the total decline from peak lending for home building construction loans continues to exceed that of other AD&C loans (nonresidential, land development, and multifamily). Such forms of AD&C lending are off a smaller 7% from peak lending. For the second quarter, the outstanding stock of these loans was approximately unchanged.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

Another interesting data point to look into would be banks AD&C loans as a percentage of capital. My suspicion is many community banks are hitting their 100% limit. Community banks are a large provider of financing for small to medium sized builders. As those bank’s approach the limit, they become less acomodating and more selective on projects and builders they will work with.