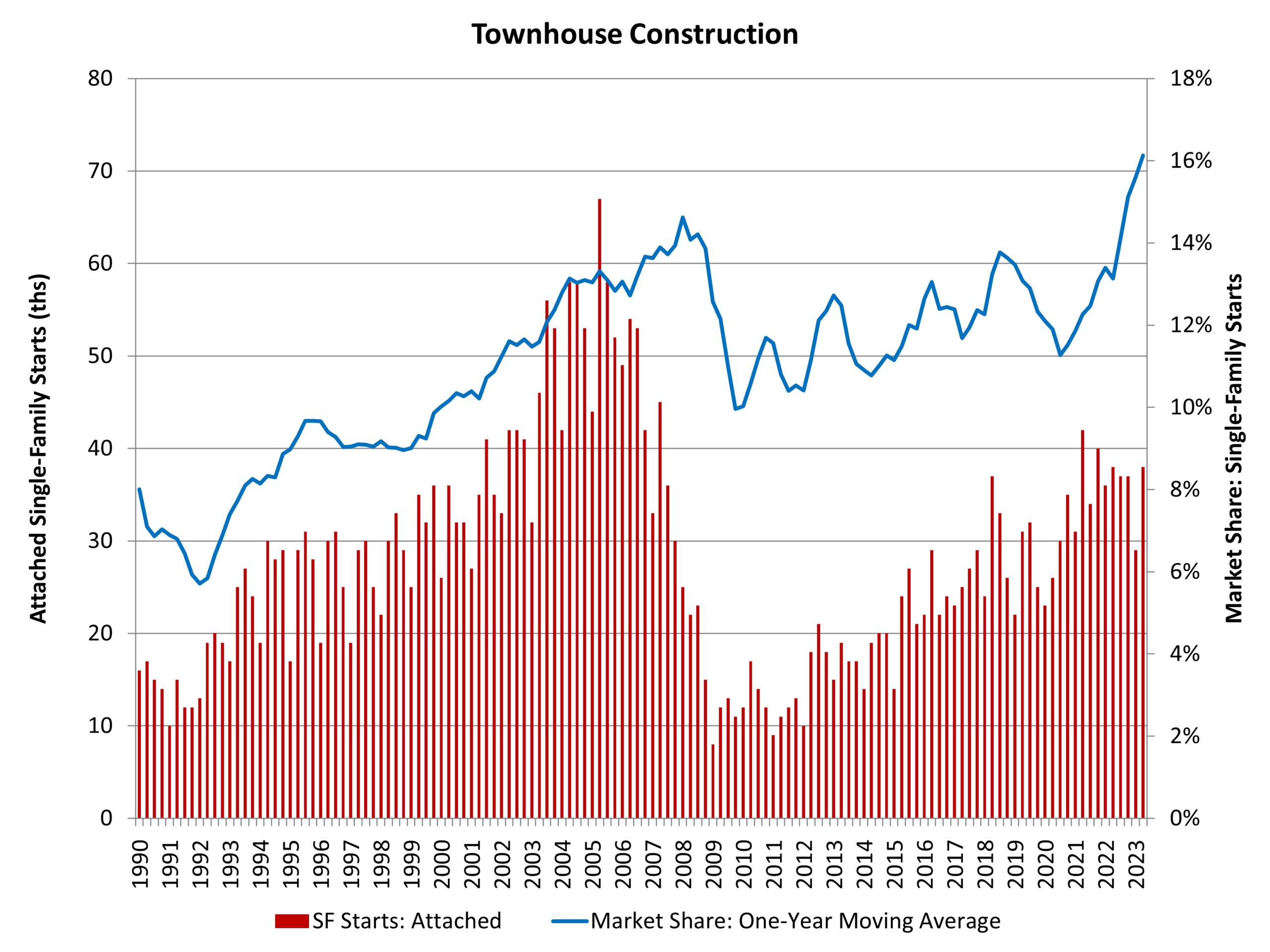

According to NAHB analysis of the most recent Census data of Starts and Completions by Purpose and Design, during the second quarter of 2023, single-family attached starts totaled 38,000, which is flat relative to the second quarter of 2022. Nonetheless, over the last four quarters, townhouse construction starts totaled a solid 141,000 homes, which is almost 5% lower than the prior four-quarter period.

Using a one-year moving average, the market share of newly-built townhouses stood at 16.1% of all single-family starts for the second quarter. Following a strong 2022, townhouse construction cooled at the start of the year, continuing its trend of lagging the broader home building market by a quarter or two. The four-quarter moving average market share is nonetheless the highest since 1985.

Prior to the current cycle, the peak market share of the last two decades for townhouse construction was set during the first quarter of 2008, when the percentage reached 14.6%, on a one-year moving average basis. This high point was set after a fairly consistent increase in the share beginning in the early 1990s.

The long-run prospects for townhouse construction remain positive given growing numbers of homebuyers looking for medium-density residential neighborhoods, such as urban villages that offer walkable environments and other amenities.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

This article highlights the stagnant trend in townhouse construction, which could have implications for construction loans as demand remains flat. Lenders may need to assess the risks carefully in this market segment.