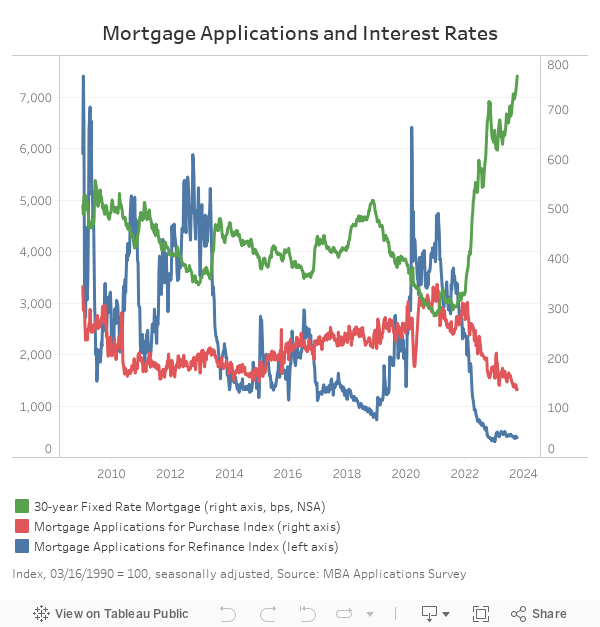

Per the Mortgage Bankers Association’s (MBA) survey through the week ending October 6th, total mortgage activity increased 0.6% from the previous week and the average 30-year fixed-rate mortgage (FRM) rate rose 14 basis points to 7.67%. The FRM rate has increased 40 basis points over the past month to its highest level since 2000.

The Market Composite Index, a measure of mortgage loan application volume, rose by 0.6% on a seasonally adjusted (SA) basis from one week earlier. Purchasing activity increased 0.6%, while refinancing activity increased 0.3% week-over-week.

Interest rates remained above seven and a half percent for the second consecutive week. The combination of increased rates and low existing for-sale inventory have continued to dismay potential buyers as the purchase index remained historically low. The seasonally adjusted purchase index was 19.4% lower than one year ago while the seasonally adjusted refinancing index was 8.8% lower than one year ago.

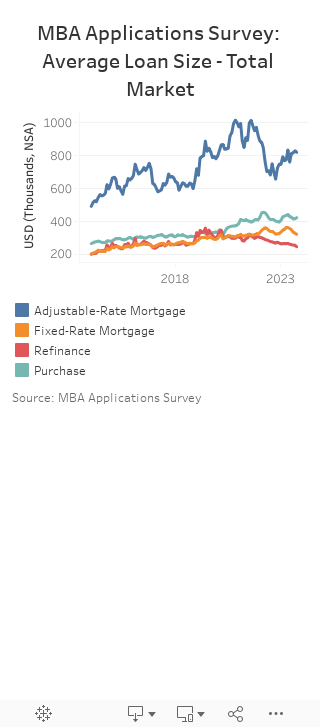

The refinance share of mortgage activity fell from 31.7% to 31.6% over the week. The adjustable-rate mortgage (ARM) share of activity rose to 9.2% from 8%, the highest share since November 2022. The average loan size for purchases was $421,600 at the start of October, down from $414,200 over the month of September. The average loan size for refinancing decreased from $254,700 over the month of September to $245,100. The average loan size for an ARM was down at start of October to $817,100 while the average loan size for a FRM fell to $320,200.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

Activity from Mortgage Rate (MR) locks performed in August and September, with closure dates in early October. The rates on the locks were probably 7% to 7.25%. 6. tenths of a 1 is not much but it is still movement.

For the construction loan sector, this indicates sustained demand for new homes and potential construction projects. Lenders might continue to offer construction loans, leveraging this market strength. Builders and developers should capitalize on this trend, seeking timely construction financing to meet the demand, ensuring that they can take advantage of the active mortgage market for their projects.