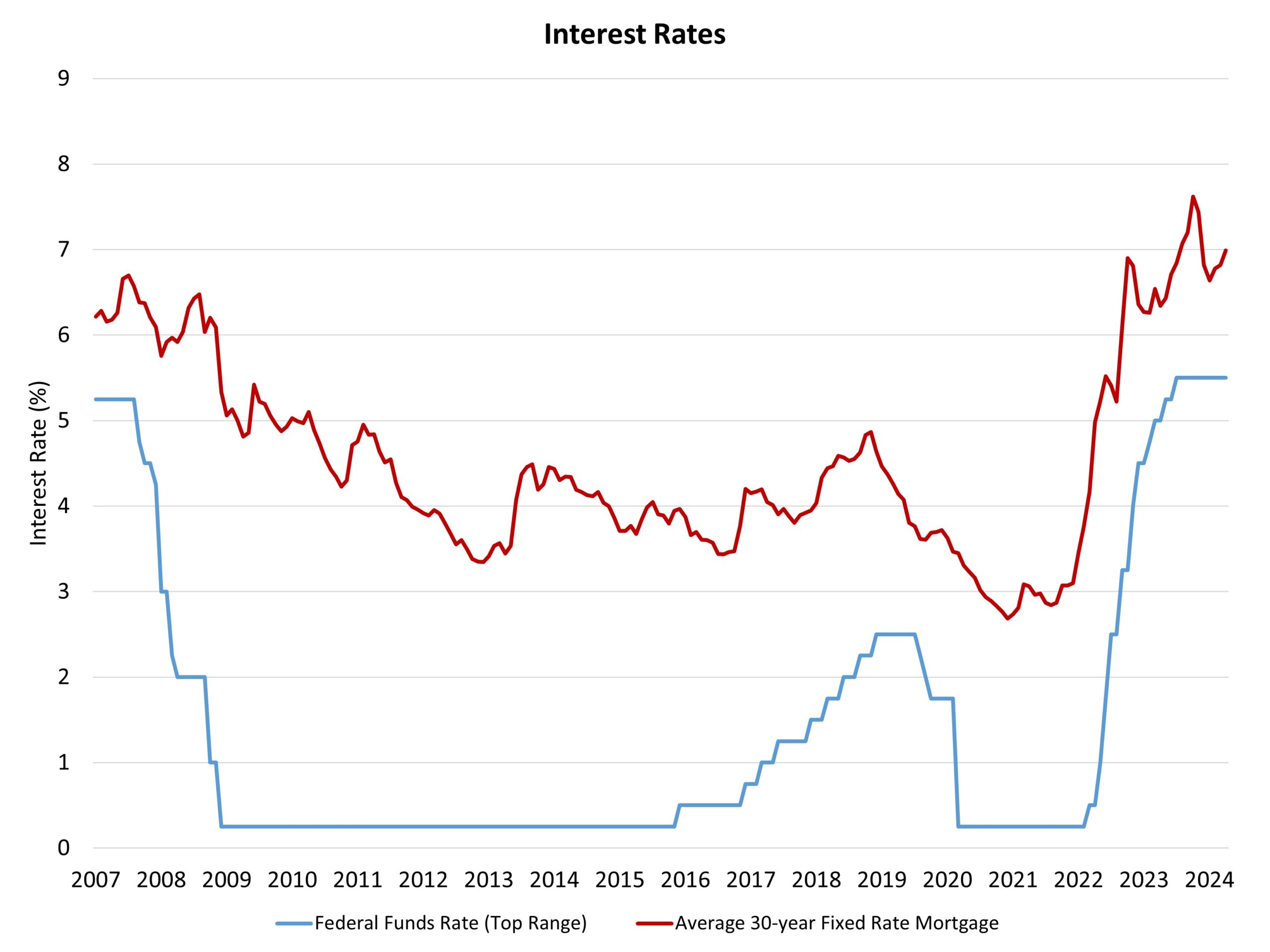

The Federal Reserve’s monetary policy committee held constant the federal funds rate constant at a top target of 5.5% at the conclusion of its April-May meeting. In its statement, the Federal Open Market Committee (FOMC) noted:

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.

The FOMC’s statement also noted:

The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.

Overall, the central bank continues to look for lower inflation readings, with the data having shown limited progress in recent months. An important reason for the lack of inflation reduction remains elevated measures of shelter inflation, which can only be tamed in the long-run by increases in housing supply. Ironically, higher interest rates are preventing more construction by increasing the cost and limiting the availability of builder and developer loans necessary to construct new housing.

Despite the ongoing policy pause, the current meeting did not tilt the Fed’s policy bias toward hawkishness. For example, Fed Chair Powell noted that an additional rate hike is all but ruled out. Powell stated at his press conference, “I think it’s unlikely that the next policy rate move will be a hike.”

Furthermore, the Fed reduced the pace of its balance sheet reduction (Quantitative Tightening), although just for Treasury bonds. It is worth noting however, this change is not being done for accommodative growth purposes but rather to manage a smooth, orderly process of balance sheet normalization. In its statement the FOMC provided details on this change:

In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities.

With inflation data moderating at a slower than expected pace and economic growth remaining solid, forecasters are pushing back the timing and number of rate cuts expected for 2024. NAHB’s current forecast continues to call for two rate cuts during the second half of 2024. However, this may be reduced to just one dependent on incoming economic data.

The NAHB Economics team’s focus continues to be on the interplay between Fed monetary policy and the shelter/housing inflation component of overall inflation. With more than half of the overall gains for consumer inflation due to shelter over the last year, increasing attainable housing supply is a key anti-inflationary strategy, one that is complicated by higher short-term rates, which increase builder financing costs and hinder home construction activity. For these reasons, policy action in other areas, such as zoning reform and streamlining permitting, can be important ways for other elements of the government to fight inflation.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.