Consumer prices in January saw the smallest year-over-year gain since October 2021 with a seventh consecutive month of a deceleration. However, this disinflation pace was much slower than expected, partially because new methodology introduces higher weights for shelter and lower weights for food and energy to reflect changes in consumer spending in 2021.

The shelter index (housing inflation) continued to rise at an accelerated pace and was the largest contributor to the total increase. Shelter inflation will primarily be cooled in the future via additional housing supply. While inflation appears to have peaked and continues to slow, inflation in core service (excluding shelter) has not begun to ease. However, real-time data from private data providers indicate that rent growth is cooling, and this is not yet reflected in the CPI data. It will be reflected in the coming months.

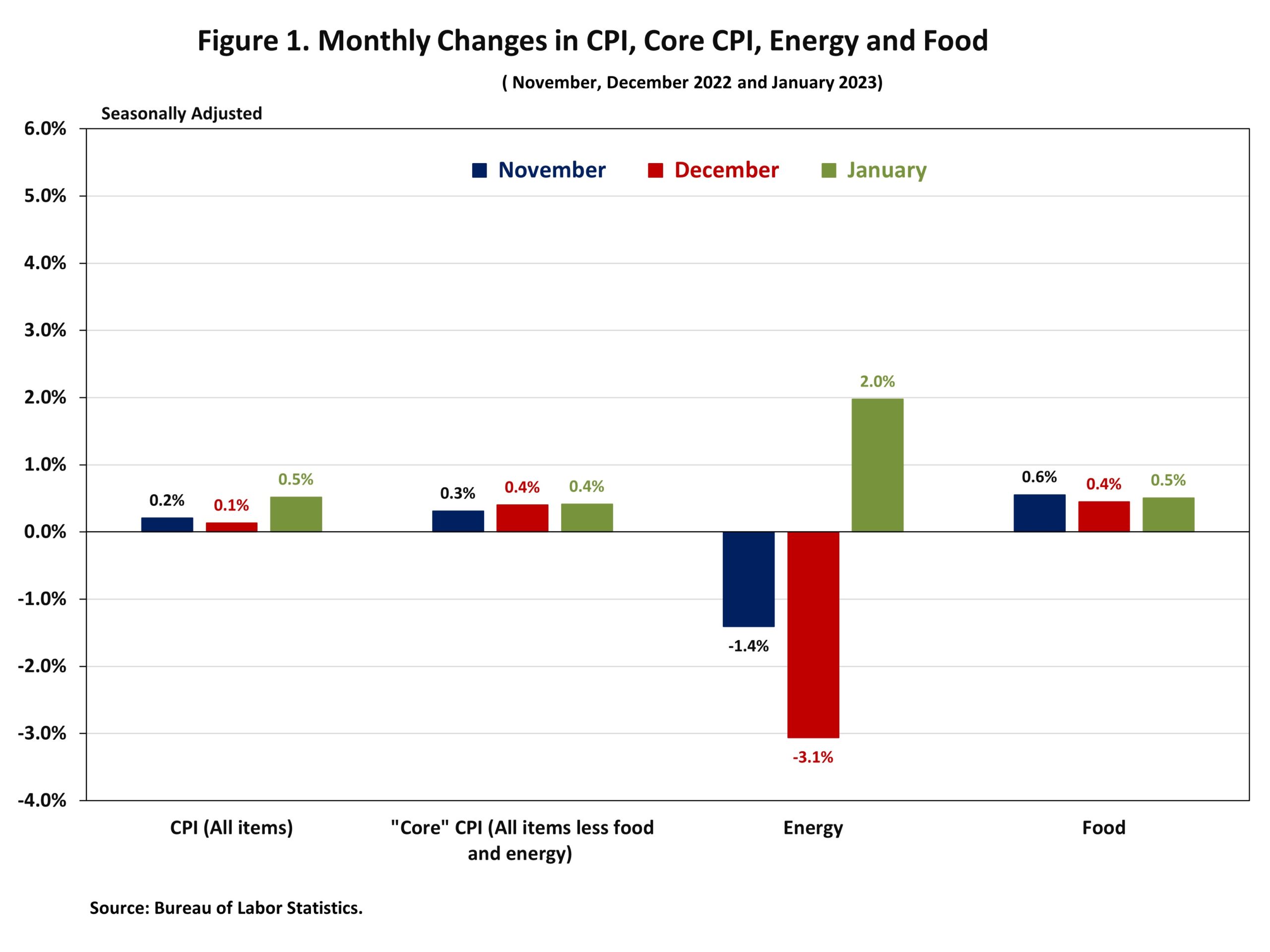

The Bureau of Labor Statistics (BLS) reported that the Consumer Price Index (CPI) rose by 0.5% in January on a seasonally adjusted basis, following an increase of 0.1% in December. The price index for a broad set of energy sources grew by 2.0% in January as the gasoline index (+2.4%), the natural gas index (+6.7%) and the electricity index (+0.5%) all increased. Excluding the volatile food and energy components, the “core” CPI rose by 0.4% in January, unchanged from last month. Meanwhile, the food index increased by 0.5% in January with the food at home index rising 0.4%.

Most component indexes continued to increase in January. The indexes for shelter (+0.7%), motor vehicle insurance (+1.4%), recreation (+0.5%), apparel (+0.8%) as well as household furnishings and operations (+0.3%) showed sizeable monthly increases in January. Meanwhile, the indexes for used cars and trucks (-1.9%), medical care (-0.4%) and airline fares (-2.1%) declined in January.

The index for shelter, which makes up more than 40% of the “core” CPI, rose by 0.7% in January, following an increase of 0.8% in December. Both the indexes for owners’ equivalent rent (OER) and rent of primary residence (RPR) increased by 0.7% over the month. Monthly increases in OER have averaged 0.7% over the last three months. These gains have been the largest contributors to headline inflation in recent months. These higher housing costs are driven by lack of attainable supply and higher development costs. Higher interest rates will not slow these costs, which means the Fed’s tools are limited in addressing shelter inflation.

During the past twelve months, on a not seasonally adjusted basis, the CPI rose by 6.4% in January, following a 6.5% increase in December. This was the slowest annual gain since October 2021. The “core” CPI increased by 5.6% over the past twelve months, following a 5.7% increase in December. The food index rose by 10.1% and the energy index climbed by 8.7% over the past twelve months.

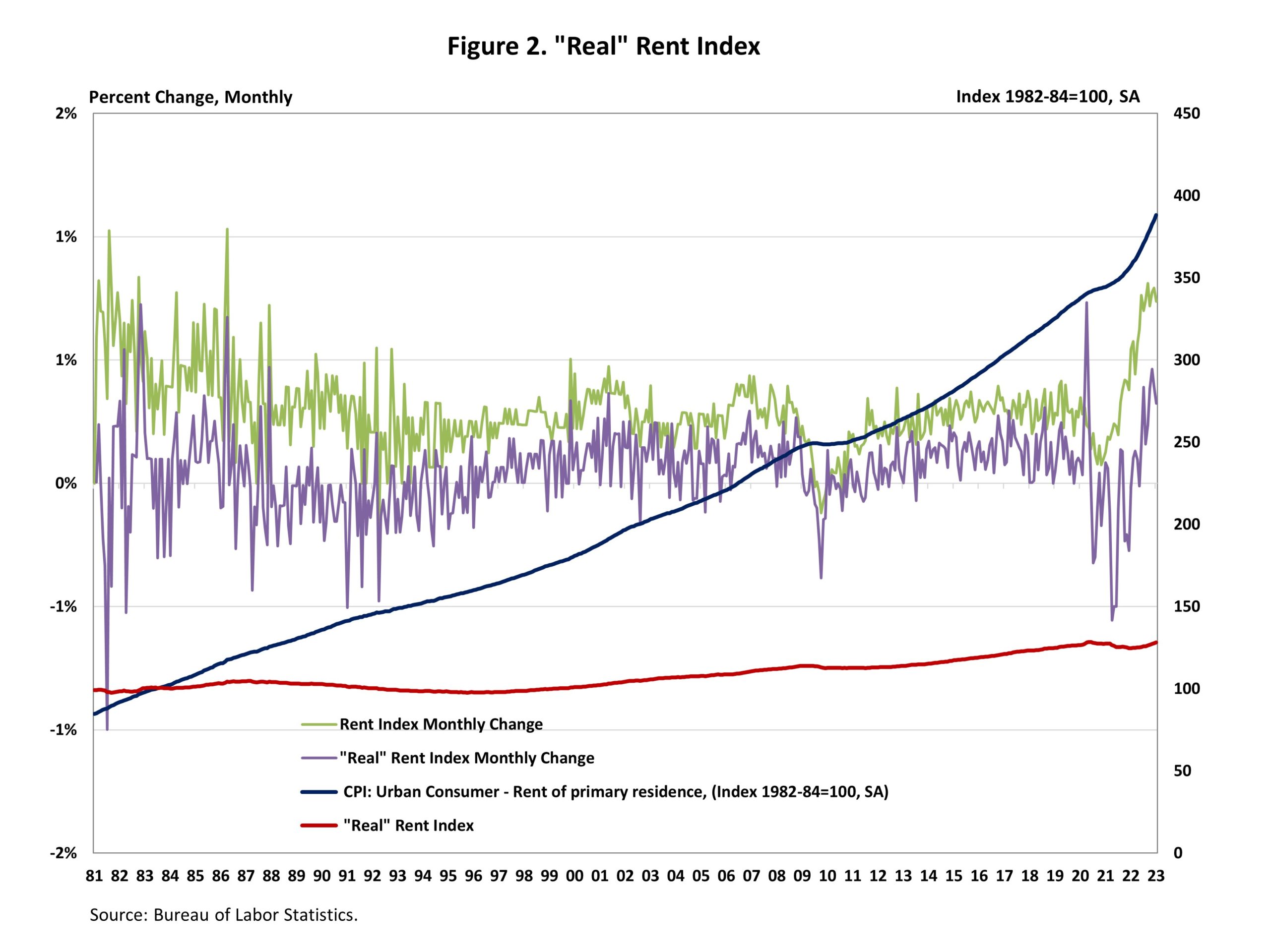

NAHB constructs a “real” rent index to indicate whether inflation in rents is faster or slower than overall inflation. It provides insight into the supply and demand conditions for rental housing. When inflation in rents is rising faster (slower) than overall inflation, the real rent index rises (declines). The real rent index is calculated by dividing the price index for rent by the core CPI (to exclude the volatile food and energy components). The Real Rent Index rose by 0.3% in January.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

Measuring the inflation rate by comparing the current rate to that of the same month in the previous year can be deceptive. If the inflation rate in the previous year was high, the rate for the current month can be deceptively low. When a period of high inflation exceeds beyond a year, I believe a more accurate indicator is to add the current inflation rate to the previous year’s rate. It is my opinion that comparing the inflation rates for the same months of 2021 and 2022 provides a much clearer picture and explains why few are feeling any improvement. Here is a sample:

October November December January

2021 6.2% 6.8% 7.0%

2022. 7.7% 7.1% 6.5% 7.5%

2023 6.4%

Total 13.9% 13,9% 13.5% 13.9%