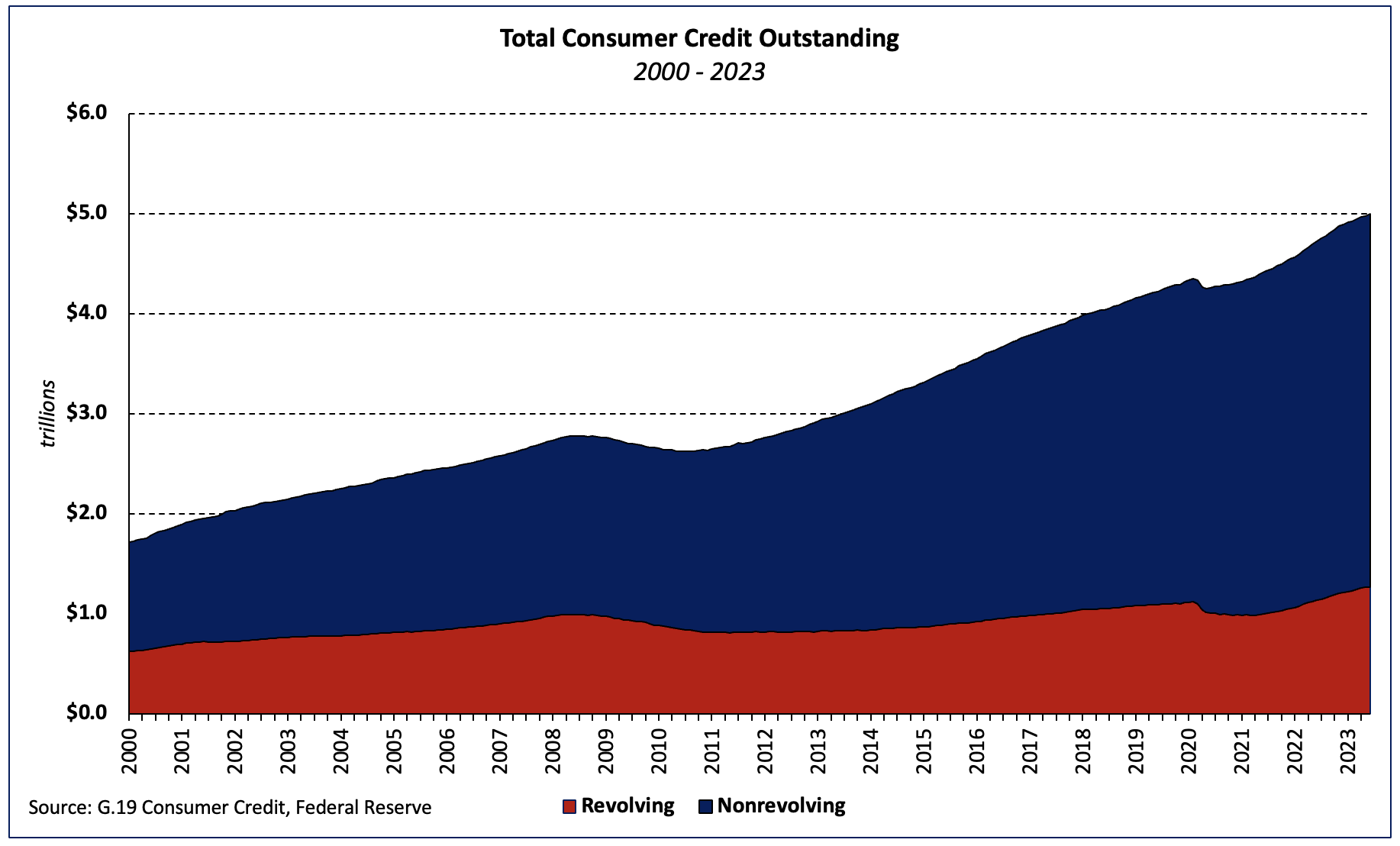

Consumer credit outstanding growth slowed to 4.0% in the second quarter 2023 (SAAR) according to the Federal Reserve’s latest G.19 Consumer Credit report, as revolving and nonrevolving debt grew at 7.1% and 3.0%, respectively. Revolving credit growth has decelerated as of late, a result of both cooling inflation and increasingly tight lending standards.

Total consumer credit outstanding stands at $5.0 trillion (break-adjusted[1] and seasonally adjusted), with $1.3 trillion in revolving debt and $3.7 trillion in non-revolving debt.

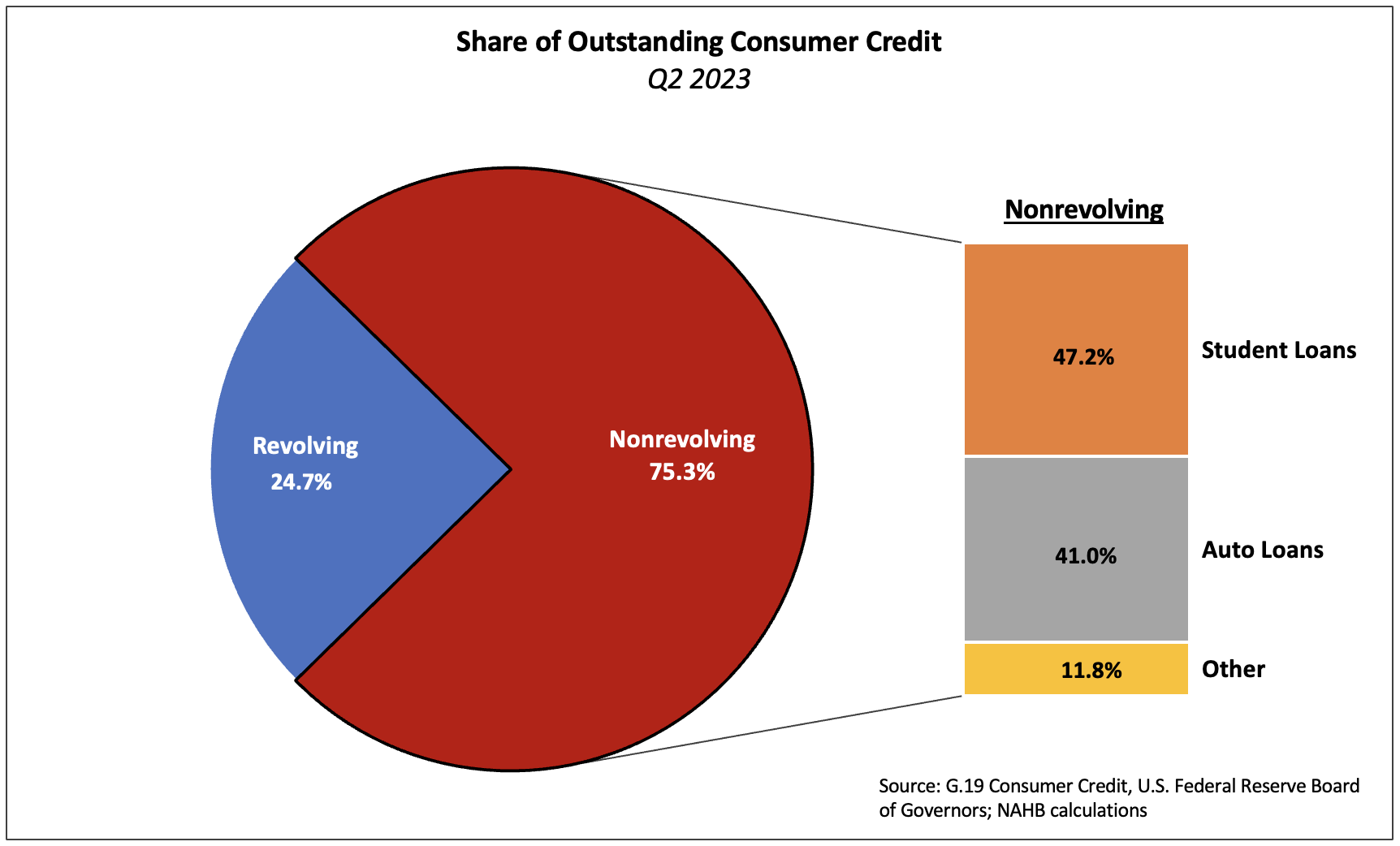

Seasonally adjusted revolving and nonrevolving debt accounted for 25.3% and 74.7% of total consumer debt, respectively. Revolving consumer credit outstanding as a share of the total decreased 0.1 percentage point over the quarter but increased 0.4 percentage point over the past year.

Auto and Student Loan Debt

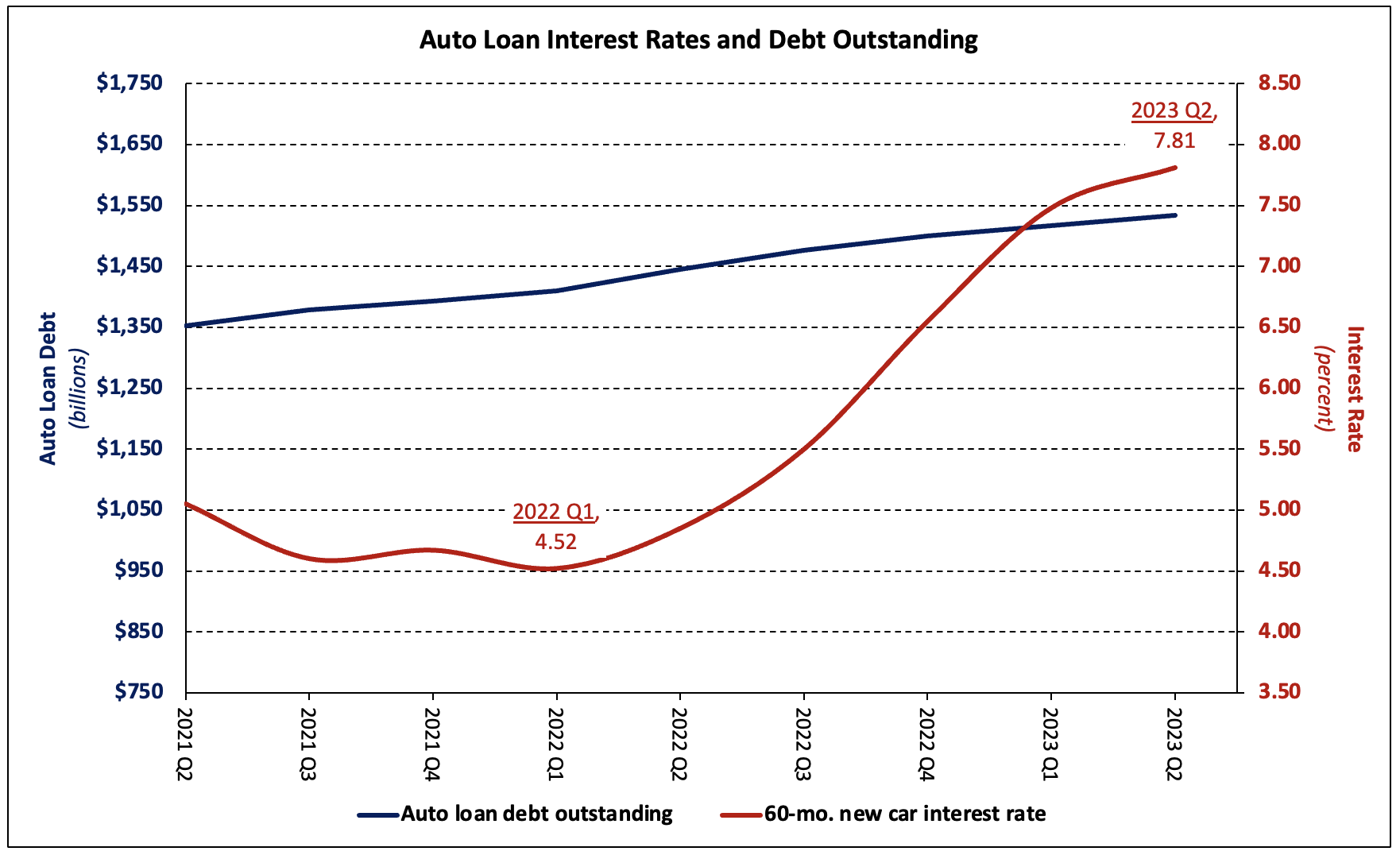

With every quarterly G.19 report, the Federal Reserve releases a memo item covering student and motor vehicle loans’ outstanding. The most recent release shows that the balance of student loans was $1.77 trillion (not seasonally adjusted) at the end of the second quarter while the amount of auto loan debt outstanding stood at $1.53 trillion (NSA).

Auto loan interest rates continued to climb as the rate for a 60-month new car loan increased to 7.81% in Q2—the highest reading since 2006. The rate has surged 3.29 ppts—more than 70%–since the Federal Reserve began the current rate hike cycle in the first quarter of 2022.

Together, student and auto loans made up 88.2% of nonrevolving credit balances (NSA)—the smallest share since 2010 and 0.5 ppt lower than the share in Q2 2022.

[1] The results of the 2020 Census and Survey of Finance Companies–delayed by the pandemic–were incorporated in the latest Consumer Credit (G.19) statistical release, resulting in large revisions dating back to June 2021. Rather than retain the large spike in credit that now appears in the raw data, we have used the “break-adjusted” historical time series developed by Moody’s Analytics and will continue to do so moving forward. Click here for more information.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

For prospective homebuilders facing evolving economic dynamics, this article underscores the relevance of construction loans. As consumer debt growth slows and lending standards tighten, construction loans can empower customers to pursue their housing aspirations with a financing option that aligns with their needs and the shifting financial landscape. In need of any construction financing, check us at builderloans.net